MES-Perspektiven 1/2012 - Quantifying the Economic Effects of a European Smart Grid

←

→

Transkription von Seiteninhalten

Wenn Ihr Browser die Seite nicht korrekt rendert, bitte, lesen Sie den Inhalt der Seite unten

MES-Perspektiven 1/2012

Quantifying the Economic Effects

of a European Smart Grid

A Survey on Costs and Benefits

Annette Knödler

Mit einem Vorwort von Franz Untersteller

MES-Perspektiven 01/2012 MES-Perspektiven 01/2012 Die MES-Perspektiven werden vom MA Europa-Studien der Europa-Universität Viadrina herausgegeben. Die MES-Perspektiven sind dem interdisziplinären Charakter des Studien- gangs verpflichtet. Sie präsentieren in loser Reihenfolge wissenschaftliche Erträge, die die Mitglieder des Studiengangs – d.h. Studierende und Dozenten – gewinnen. Ein besonderes Augenmerk wird dabei auf solche politische, rechtliche und wirtschaftliche Prozesse des europäischen Integrationsprozesses gelegt, die disziplinäres Wissen herausfordern und weiterentwickeln. Über die Autorin Annette Knödler ist Referentin für Umwelt, Klima und Energiewirtschaft in der Vertretung des Landes Baden-Württemberg bei der EU in Brüssel. Im Jahr 2011 schloss sie den Mas- terstudiengang „European Studies“ an der Europa Universität Viadrina Frankfurt/Oder ab. Zuvor studierte sie Politikwissenschaften und Französische Philologie am Otto-Suhr-Institut der Freien Universität Berlin. Ihr Interesse für Klima- und Energiepolitik entdeckte und ver- tiefte sie unter anderem bei ihrer Tätigkeit als Praktikantin beim Worldwatch Institute in Washington D.C. und als Werkstudentin der EnBW Energie Baden-Württemberg AG in Ber- lin. Annette Knödler widmet sich Fragen der europäischen Energiepolitik und beschäftigt sich mit der Transformation des Energiesystems sowohl auf globaler als auch auf regiona- ler Ebene. Betreuer Erstgutachter Prof. Dr. Reimund Schwarze Zweitgutachter Dr. habil. Jörg Jasper Herausgeber der Reihe MES-Perspektiven Prof. Dr. Timm Beichelt, Prof. Dr. Carsten Nowak, Dr. Nicolai von Ondarza, Prof. Dr. Reimund Schwarze Kontakt Professur für Europa-Studien Europa-Universität Viadrina Postfach 1786 15207 Frankfurt/Oder Redaktion dieser Ausgabe Lisa Magdalena Richter Erscheinungsdatum 16. April 2012

MES-Perspektiven 01/2012 Kurzzusammenfassung Diese Arbeit untersucht, ob die Einführung eines europaweiten Smart Grid, bestehend aus einem Verbund nationaler intelligenter Stromnetze, wirtschaftlich lohnenswert ist. Zu diesem Zwecke erfolgt eine Untersuchung zehn nationaler Kosten-Nutzen-Analysen, die entweder nur die Einführung intel- ligenter Stromzähler oder die Errichtung nationaler intelligenter Stromnetze thematisieren. Intelligen- te Stromzähler werden als notwendige Voraussetzung für die Schaffung eines intelligenten Strom- netzes unter Einbeziehung privater Haushalte angesehen. Aus diesem Grund ist auch die Analyse dieser Studien mit begrenztem Anwendungsbereich sinn- voll. Die Studien werden auf Art, Höhe und Verteilung der jeweiligen Kosten- und Nutzen-Parameter untersucht. Obwohl Verteilungseffekte kein Gegenstand klassischer Kosten-Nutzen-Analysen sind, ist die Betrachtung selbiger für diese Arbeit bedeutsam. Denn nur so können Handlungsempfehlun- gen an die Politik formuliert werden, die den Akteuren mit den höchsten finanziellen Bürden staatli- che Anreizregulierungen anbieten. Um die Analyse der Kosten und Nutzen eines intelligenten Stromnetzes zu festigen, werden darüber hinaus eigene Berechnungen angestellt. Diese untersuchen einerseits den Energieeinsparungsef- fekt, welcher durch Smart Grids in privaten Haushalten entsteht und zum anderen den Kapazitätsef- fekt, der die Reduzierung von Grenzkapazitäten durch Lastverlagerung zu off-peak-Zeiten monetär bewertet. Schließlich werden die Kosten für den Infrastrukturausbau der Stromnetze betrachtet. Die- ser Arbeit liegt die Annahme zugrunde, dass das Energiesystem der Zukunft in der Lage sein muss einen hohen Anteil von erneuerbaren Energien einzuspeisen. Daraus wird die These abgeleitet, dass die Kosten eines sogenannten Dumb Grid mit einem hohem Anteil erneuerbarer Energien im Energiemix höher sind als die eines Smart Grid, da durch die intelli- gente Vernetzung Synergien ausgenutzt werden, Lastverschiebung stattfinden kann und somit weni- ger Infrastrukturausbau nötig ist. Unter der Prämisse, dass in Zukunft erneuerbare Energiequellen einen signifikanten Anteil am Energiemix haben werden, schaffen Smart Grids demnach einen Op- portunitätsnutzen gegenüber einem Dumb Grid.

MES-Perspektiven 01/2012 Table of Contents 1. Introduction .. 2 2. Definitions 4 2.1 Context of this StudyEEEEEEEEEEEEEEEEEEEEEEEEE. 4 2.2 Definition and Functioning of Smart GridsEEEEEEEEEEEEEEEEE.. 6 3. Research Question and Hypothesis .. 7 4. State of Research .... 9 4.1 Literature Review. EEEEEEEEEEEEEEEEEEEEEEEEEEE. 9 4.2 State of Politics.EEEEEEEEEEEEEEEEEEEEEEEEEEEE.. 11 5. Costs and Benefits of Smart Grids in a European Context 18 5.1 Method: Cost-Benefit-AnalysisEEEEEEEEEEEEEEEEEEEEEE. 18 5.2 Data and ProcessingEEEEEEEEEEEEEEEEEEEEEEEEEE.. 21 5.3 Analysis of National CBAsEEEEEEEEEEEEEEEEEEEEEEE.... 22 5.4 Estimates about a Europe-wide Smart GridEEEEEEEEEEEE.EEEE 38 6. Summary and Policy Recommendations . 46 7. References 51 7.1 BibliographyEEEEEEEEEEEEEEEEEEEEEE.............................. 51 7.2 InternetEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE. 59 Annex ... 63

MES-Perspektiven 01/2012

Table of Figures

Figure 1 Expected Surplus in Generation Capacity (Blue) and Need for Additional 4

Capacity (Red) in 2020, in the Case of Germany (dena 2011:4)

Figure 2 Electricity Flows in a Traditional and Future Electricity Network (own 6

graph, based on EnBW 2011)

Figure 3 Vision of a European Super Smart Grid (Energynautics 2011:9) 6

Figure 4 Main Aspects of Smart Grids and Added Value of This Study (own graph) 8

Figure 5 Opportunity Benefits for Smart Grids (own graph) 8

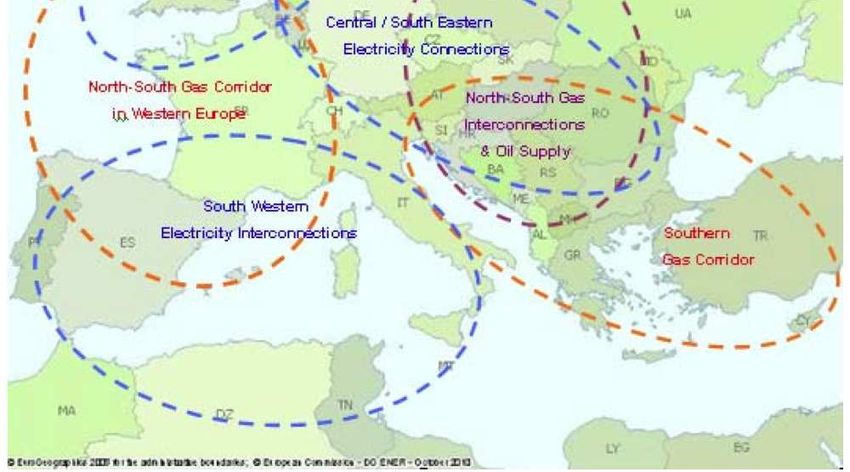

Figure 6 Priority Corridors for Electricity, Gas and Oil (COM(2010)677/4:20) 13

Figure 7 Overview of National CBAs (own graph) 23

Figure 8 Overview Study Designs (own graph) 24

Figure 9 Scenarios for Austria (PWC) (own graph) 26

Figure 10 Comparison of the Macroeconomic Effects (PWC 2010:12) 26

Figure 11 Scenarios for the Netherlands (Kema) (own graph) 27

Figure 12 Scenarios for Hungary (A.T. Kearney) (own graph) 27

Figure 13 Scenarios for the United Kingdom (DECC) (own graph 28

Figure 14 Scenarios for the Netherlands (Frontier) (own graph) 28

Figure 15 Cumulative NPV Impact of a Smart Meter Roll-Out (Frontier 2008:58) 28

Figure 16 Scenarios for the United Kingdom (ENSG) (own graph) 29

Figure 17 Scenarios for Germany (Kema) (own graph) 29

Figure 18 Scenarios for Germany (Frontier) (own graph) 30

Figure 19 Scenarios for Austria (Capgemini) (own graph) 30

Figure 20 Scenarios for Denmark (energinet) (own graph) 31

Figure 21 Comparison of BAU and Smart Grid Scenario (Energinet 2009:16) 31

Figure 22 Cost and Benefit Parameters (own graph) 33

Figure 23 Amounts of Costs and Benefits (own graph, based on ATK 2010, 35

Energinet 2010, Kema 2010, PWC 2010, DECC 2011)

Figure 24 Effects of the Austrian CBA for Each Scenario (PWC 2010:8) 36

MES-Perspektiven 01/2012

36

Figure 25 Net Present Values of a Smart Meter Roll-Out in Austria (Capgemini

2010:66)

Figure 26 Distribution of the Net Present Costs and Benefits in the Netherlands 37

(Kema 2010:48)

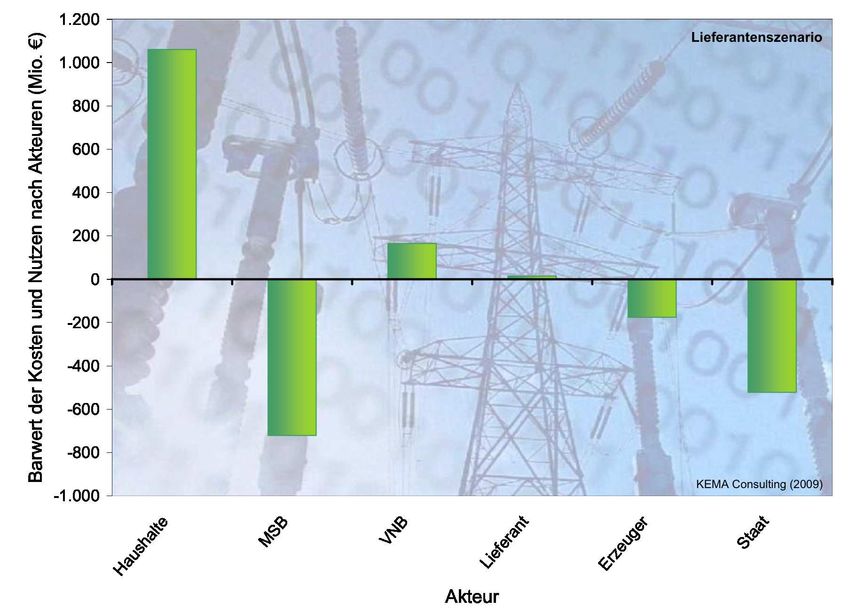

Figure 27 Net Present Value of the Costs and Benefits for a Smart Meter Roll-Out 37

in Germany (Kema 2009:210)

Figure 28 Distribution – Overall NPV and Industrial NPV in the Hungarian Case 38

(ATK 2010:72)

Figure 29 Investment Costs for Transmission Grid Infrastructure with High RES 40

Integration (own graph, based on Greenpeace 2009, ENTSO-E 2010,

IEA 2010, Energynautics 2011)

Figure 30 Investment Costs for Transmission and Distribution Grid Infrastructure 41

with High RES Integration (own graph, based on dena 2005, dena

2010, COM (2010)677/4, bdew 2011, DB Research 2011)

Figure 31 Comparison of Annual Infrastructure Investment Costs (own graph, 42

based on dena 2005/2010, Greenpeace 2009, COM(2010)677/4, EN-

TSO-E 2010,IEA 2010, bdew 2011,Energynautics 2011)

Figure 32 Capacity Effect (Load Shift Aspect) (own graph) 44

Figure 33 Energy Effect (Energy Savings Aspect) (own graph) 45

Figure 34 Opportunity Benefit for Smart Grids in the Long Run (own 49

graph)

MES-Perspektiven 01/2012 Abbreviations a Annually ACER Agency for the Cooperation of Energy Regulators ATK A.T. Kearney Ges.m.b.H. CBA Cost-Benefit-Analysis CCGT Combined Cycle Gas Turbine CCS Carbon Capture and Storage CH Switzerland cf. Confer (lat.) CO2e Carbon dioxide equivalent COM European Commission DER Distributed Energy Resources DG Directorate-General DR Demand response DSM Demand side management DSO Distribution System Operator (=VNB, Verteilnetzbetreiber) EEG Renewable Energy Sources Act (Erneuerbare-Energien-Gesetz) EEWärmeG Renewable Energy Heat Act Engl English ENTSO-E European Network of Transmission System Operators for Electricity ENSTO-G European Network of Transmission System Operators for Gas EP European Parliament ETS Emission Trading Scheme EU European Union EU27 European Union (with current 27 member states) EU27+2 EU27 including Norway and Switzerland EUR Euro FiT Feed-in Tariff GHG Greenhouse Gases GW Gigawatt (109 Watt) HEO Hungarian Energy Office HVDC High Voltage Direct Current Transmission transmission ibid. Ibidem (lat.) ICT Information and Communication Technology

MES-Perspektiven 01/2012

IEA International Energy Agency

ISO Independent System Operator

IT Information Technology

ITO Independent Transmission System Operator

KW Kilowatt (103 Watt)

lit. Littera (lat.)

MEUR Million Euro

MPO Metering Point Operator (=MSB, Messstellenbetreiber)

MW Megawatt (106 Watt)

n.d. No data

neg Negative

NPV Net Present Value

OCGT Open Cycle Gas Turbine

OECD Organization for Economic Co-operation and Development

O&M Operation and Maintenance

PHEV Plug-In Hybrid Electric Vehicles

pos Positive

PWC PricewaterhouseCoopers

PV Photovoltaic cells

RE Renewable Energies

RES Renewable Energy Sources

RO Renewables Obligation

RQ Research Question

SETIS Strategic Energy Technologies Information System (European Commis-

sion)

SM Smart Metering

SG Smart Grid

StrEG Feed-In-Act (Stromeinspeisegesetz)

TEU Treaty on European Union

TFEU Treaty on the Functioning of the European Union

TSO Transmission System Operator

TYNDP Ten Year Network Development Plan

V2G Vehicle to Grid

VEÖ Verband der Elektrizitätswerke Österreichs

MES-Perspektiven 01/2012

Foreword change. Thinking of demand side manage-

ment, this can only function if consumers

change their behavior and new business

models including flexible tariffs enter the

“How to transform our energy system?” This

market.

is the question dominating the current debate

in climate and energy politics - from a political

and scientific but also an economic perspec- The transformation of our energy system

tive. The way to a sustainable and low- is imperative, indispensable and irreversible.

carbon future holds enormous challenges to The Land Baden-Württemberg wants to be

overcome and tremendous changes to ac- the leading region for energy and climate

complish. One key measure identified is to protection within Germany and within the EU.

dramatically expand our production of RES - Therefore Baden-Württemberg pursues the

a path we already commenced on, but need development of an integrated concept for

to go way further. To continue changing our energy and climate protection. This concept

electricity production, the key challenge is on includes the irreversible phase-out of nuclear

how to integrate a high amount of RES into energy while maintaining supply security,

the electricity grid, thus helping to overcome fostering energy efficiency and energy sav-

a lack of storage capacities and at the same ings, expanding RES, and integrating flexible

time being economically efficient. gas power plants for the changed energy

mix. Furthermore, Baden-Württemberg aims

at adapting the grid infrastructure to the

The idea of a Smart Grid put in place to

changed power plant fleet.

manage a secure feed-in of fluctuating power

flows is on everybody’s lips. This idea is very

appealing as it would allow the interaction of However, a regional focus is not sufficient

all users connected to the grid, such as pro- in this regard. Baden-Württemberg may be a

ducers, consumers and those that do both. forerunner providing ideas for others to fol-

While a number of studies focusing on the low, but to establish a low carbon and high

upgrading and modernizing of national elec- renewable environment the joint action of

tricity grids exists, surprisingly the European many is needed – within a European ap-

perspective is missing. But secure, sustaina- proach. Only if all members of the European

ble and affordable energy of the 21st century Union act together, interconnect their electric-

without a close collaboration within the EU ity grids and foster RES, we will be able to do

seems hardly possible. The present thesis the urgent, but giant step forward.

takes up the European perspective and links

it to core challenges. It investigates whether

the deployment of a European Smart Grid

would be cost-efficient compared to a con- Franz Untersteller MdL, Minister for the Envi-

ventional “Dumb Grid” adapted to a high ronment, Climate Protection and the Energy

share of RES. The thesis shows that we can Sector Baden-Württemberg

have a real benefit in establishing an inter-

connected European Smart Grid, adapted to Stuttgart, January 2012

integrate a necessary high share of RES.

The “MES Perspektiven“ provides a plat-

form for excellent final studys of the Master

Program “European Studies”. The present

Master thesis constitutes the second edition

of the “MES Perspektiven” and may set the

path for an in-depth discussion of highly val-

uable theses that otherwise would only hardly

gain the attention they actually deserve within

science, politics and the general public. The

Master of European Studies (MES) of the

European-University Viadrina Frankfurt

(Oder), Germany, distinguishes itself by its

interdisciplinary, so does the broader topic of

this present thesis. If we want to transform

our energy system, not only the infrastruc-

ture, but also the habits of the people need to

1

MES-Perspektiven 01/2012

1. Introduction and distribution lines (Oettinger 2011a:3).

The result would be a Dumb Grid, a so-called

Today the often-cited 20-20-20 goals of the “copperplate” which would be over-sized to

European Union (EU) belong to the everyday avoid congestion, “comparable to building

vocabulary of media, scientists and politi- four- or five-lane automobile highways to

cians. Nevertheless, the realization of this avoid potential congestion hours” (Eurelectric

prospect still lacks action. If just the goal of 2011a:9). The second option would be the

20% renewable energy – as one of the three establishment of a Smart Grid, which can

targets – shall be realized until 2020, a fun- feed-in, transport and distribute electricity

damental change in the European energy more efficiently through bidirectional infor-

system has to happen in next to no time: “We mation and communication technologies

are currently going through a paradigm shift (ICT) between producers and generators and

in the way we produce, transmit, distribute therewith could “limit the need for new lines”

and trade energy“ (Oettinger 2011a:3). (Eurelectric 2011a:9).

Various signs are already pointing to In that regard, this study develops the hy-

change. The nuclear catastrophe of Fuku- pothesis that the establishment of a Europe-

shima in mind, Germany’s government de- an Smart Grid will be worthwhile as the op-

cided in June 2011 to phase-out its nuclear portunity costs for adapting a Dumb Grid to

power until 2022. Already one year earlier the the integration of a high share of RES would

German Federal Environment Agency pub- be even higher. This vision is also shared by

lished a report stating that 100% renewable the European Commission that finds that

electricity is feasible by 2050 (cf. Umwelt- “Smart Grids will be the backbone of the fu-

bundesamt 2010). It was joined by the 2010 ture decarbonised power system” (COM(20

PWC study 100% Renewable Electricity – a 11)202:2). This study follows the definition of

Roadmap to 2050 for Europe and North Afri- the European Union’s Smart Grid Task Force

ca (cf. PWC 2010b). It is not only Germany, whereas a Smart Grid is “an electricity net-

the traditional European climate change fore- work that can cost efficiently integrate the

runner, but also its European neighbours that behaviour and actions of all users connected

proceed to action: in May 2011, the United to it – generators, consumers and those that

Kingdom announced to cut greenhouse gas do both” (M/490:2).

(GHG) emissions by 50% compared to 1990

levels in the period 2023-20271. Three To this end, this study examines the costs

months earlier, Denmark declared in its En- and benefits of a European Smart Grid.

ergy Strategy 2050 the objective to be inde- However, since the energy mix and the “gen-

pendent from fossil fuels as of 2050 (cf. KE- eral structure” of the energy system are still

MIN 2011:5). in the legislative power of the EU member

states, the establishment of a harmonized

In order to reach these ambitious goals, single European Smart Grid is not feasible

the European energy mix has to include a yet (cf. TFEU Art. 194). Therefore, within the

significant amount of renewable energy scope of this study, a European Smart Grid is

sources (RES). The topmost challenge of defined as 27+2 (including Norway and Swit-

RES is their intermittency, which entails fluc- zerland) national Smart Grids that are inter-

tuating power flows that negatively affect grid connected. The contribution to the debate on

stability and security of electricity supply. EU energy policy of this study is to quantify

Regarding the European electricity grid there the establishment of such a Smart Grid,

are two possible solutions to meet intermit- which any study has – surprisingly in contrast

tency and to feed-in a high share of RES2. to the fact of serious time pressure – covered

so far. Accordingly, the research questions

The first possibility is to expand the exist- (RQ) guiding this study are:

ing grid, which is “too old, too fragmented,

and already overloaded at several critical (1) Will the establishment of a European

points” by simply laying more transmission Smart Grid be cost-effective?

(2) How are the costs and benefits dis-

tributed among market actors?

1

Cf. URL DECC (2011): Fourth Carbon Budget: Oral (3) What are the opportunity benefits of a

Ministerial Statement by Chris Hune – 17 May 2011. Smart Grid compared to a Dumb Grid

2

This paper will focus on the European electricity sup- adapted to integrate a high share of

ply, not on energy in general RES?

2MES-Perspektiven 01/2012

Energy policy and the security of energy impacts are not a core part of CBAs, it will be

supply will shape our future, especially if important to consider this aspect in order to

western countries want to preserve their ac- enable policy recommendations for incentive

cumulated wealth without further endanger- regulation to ease the establishment of a

ing the world’s climate. Our energy world is European Smart Grid.

changing fundamentally, some even speak of

a revolution, which at least can be seen as a As those ten studies have their main fo-

major turning point in the way we generate cus on Smart Metering, the second part of

the key resource energy. Furthermore, con- the empiric analysis focuses on the econom-

sidering the nuclear catastrophe in Fukushi- ics of a Smart Grid. Accordingly, this section

th

ma in the year of the 25 anniversary of is divided into the quantification of its costs

Chernobyl, it becomes obvious that renewa- (1) and its benefits (2). As only very limited

ble energy sources are the future as dangers information is available for the second as-

of nuclear energies can never be fully con- sessment, own calculations will be used

trolled. It is just a question of bridging tech- here. The main costs that occur are costs for

nologies, and the feasibility of this new ener- modernizing the grid infrastructure. Eight

gy world. For lack of robust research quanti- different studies will be tested for the overall

fying the economic effects of a European and annual costs that occur when updating

Smart Grid – which is indispensable for inte- and newly building parts of the electricity grid

grating a significant share of RES – a secure to integrate a high share of RES. The per-

basis for future decisions that need to be centage of the existing grid that is affected by

taken in the EU has to be prepared. this development will be assessed too. The

two main benefits occurring with a Smart Grid

The study is structured as follows: At first, deployment are then a capacity effect as well

the definition and functioning of Smart Grids as an energy effect. Within the capacity effect

is explained, the topic is embedded in a wider the peak load capacity of power plants in the

context and the key technologies enabling a merit order, which may be reduced by 2,5%

Smart Grid are presented (Chapter 2). This is to 7,5% through load shift to off-peak times,

followed by the formulation of the hypothesis is quantified monetarily. The latter effect val-

and the research questions; here it will also ues the expected end energy savings of

be elaborated why this study is a contribution households that are also tested with a sensi-

to the existing knowledge about Smart Grids tivity from 2,5% to 7,5%.

(Chapter 3). The last section of the theoreti-

cal part will be an overview of the latest state In sum, findings of the study are that while

of the art; the existing scientific literature will a short-term perspective the Dumb Grid solu-

be reviewed, and the state of policies con- tion may be less expensive (lower capital

cerning Smart Grids will be presented. First expenditures in ICT, cf. Eurelectric 2011a:9),

the policies of the European Union will find but in the long run the benefits of a Smart

detailed consideration, secondly an introduc- Grid will outweigh its costs (better allocation

tion of the national policies of those six coun- of resources, end energy savings, reduced

tries, that will be part of the analysis, follows peak capacity through load shift (cf. Eurelec-

(Chapter 4). tric 2011a:9). The conclusion part also gives

policy recommendations for incentivizing the

This is followed by the empiric analysis establishment of a European Smart Grid and

(Chapter 5). In the first place an introduction gives an outlook to further research.

in the method of cost-benefit-analyses is

given, and the data and its processing are

presented. The subsequent analysis is then

two-fold. The first part focuses on the cost-

effectiveness of a Smart Meter roll-out, which

is understood to be constitutive for the estab-

lishment of a Smart Grid that includes

households. This section will be a survey on

ten national CBAs that either quantify a

Smart Metering roll-out or the establishment

of a Smart Grid. The analysis will focus on

the applied cost and benefit parameters, their

amount, as well as their distribution among

market actors. Even though distributional

3MES-Perspektiven 01/2012

2. Definitions

2.1 Context of this study

The centre of all reflections is the proposition

that a future energy network must be capable

to feed-in a significant amount of renewable

energy sources (RES) guaranteeing a secure

energy supply at all time.3

Therefore, the existing European electrici-

ty grid has to meet two main challenges:

First, the expansion of existing grid infrastruc-

ture in order to be able to transport renewa-

bly generated energy from areas with a high

solar or wind potential to areas with less po-

tentials but higher energy demand (see Fig-

ure 1). Second, the grid has to be made

smart to outbalance the intermittency of RES

through the detection of overload and

through an intelligent distribution of the elec-

tricity to guarantee grid stability. Generally,

the following assumption seems to be evi-

dent: the smarter the grid the less grid infra-

structure or new capacity is needed, because

Figure 1 Expected Surplus in Generation Capacity

synergies and bi-directional communications

(Blue) and Need for Additional Capacity (Red) in

allow exploiting the grid capacities in the 2020 in the Case of Germany (dena 2011:4).

most optimal way.

teen nuclear power plants were shut down

Thus, the objective would be the deploy- temporarily5.

ment of a Europe-wide Smart Grid that con-

sists of 27 (or 27+2, including Norway and

In June 2011, after a three-month morato-

Switzerland) national Smart Grids that are

rium, the German government decided to

interconnected with each other.4 The vision of

phase-out nuclear power by 2022 and to

a single European Smart Grid will stay a vi-

decommission the seven nuclear plants in

sion, however, until the EU adopts a common

question6 In consequence, Germany’s energy

energy policy. Although the Treaty on the

system is confronted with a loss of 7GW ca-

Functioning of the EU (TFEU) encourages

pacity, which forces the country to import an

the adoption of EU legislation in order to

increased amount of electricity7. The solution

promote the interconnection of energy net-

of this problem is twofold: First, more RES

works, the functioning of the energy market,

must be integrated, and second, new fossil

and the expansion of RES and energy effi-

power plants (predominantly gas plants)

ciency, the energy mix and “the general

need to be built in order to meet intermittency

structure” of the member states’ energy sup-

ply remain within national legislative powers

(TFEU Art.194).

The nuclear crisis in Japan, caused by a 5

As a reaction to the nuclear crisis in Fukushima, the

historic earthquake and a tsunami in March German government issued a moratorium of three

months for its seven oldest nuclear power plants, begin-

2011, opened a new window of opportunity

ning March 15th, 2011. During these three months the

for action. In Germany, seven out of seven- nuclear power plants shall undergo a stress test focusing

on the plants’ safety standards (cf. URL Bundesregier-

ung (2011): Kernkraftwerke kommen auf den Prüfstand).

3 6

The EU has the objective to reach 20% renewables by Cf. URL Bundesregierung (2011): Ausstieg aus der

2020, Germany declared to increase the share of RES in Kernkraft in einem Jahrzehnt.

gross energy consumption up to 60% by 2050 (cf. 7

COM(2007)1, cf. BMU/BMWi (2010)). As of March 17th 2011, Germany imports 50GWh on a

daily basis, so that the current flows from France and the

4

Hereinafter the term European Smart Grid will conse- Czech Republic doubled (cf. URL bdew (2011): Entwick-

quently describe 27+2 interconnected national Smart lung von Stromerzeugung und Stromaustausch).

Grids

4MES-Perspektiven 01/2012

and provide peak capacity8 This example levels, but may be needed to transported

illustrates further how declining capacity of long distances to another region before finally

fossil fuel power plants combined with an reaching the end consumer (see Figure 2).

expansion of RES jeopardizes the grid stabil- The existing system faces two main chal-

ity and the security of energy supply. Even lenges: First, the modernization of the grid

though Germany is a forerunner pursuing infrastructure in order to manage the in-

RES, while most of its European neighbours creased power flows and second the estab-

are more reluctant, all EU member states lishment of bidirectional communication be-

have agreed on the 20-20-20-targets, aiming tween generator, distributor and consumer so

for a share of 20% RES in 2020 (cf. that peaks and troughs can be outbalanced.

COM(2007)1).

The traditional energy system followed the

2.2 Definition and Functioning of Smart Grids principle of supply follows demand. If the

demand increased, centralized power plants

were switched on in line with the merit-order

RES cannot constantly provide energy since curve. In a system with a lot of intermittent

especially solar and wind power rely on me- RES and decentralized generation, there will

teorological circumstances and are thus peri- be a paradigm shift to demand follows supply

odically fluctuating. Provided that a high (cf. Eurelectric 2011b:4-15). This implies that

share of intermittent renewable energy in times of high supply (e.g. strong wind)

sources need to be integrated in the electrici- smart appliances in households are automat-

ty grid, a Smart Grid becomes indispensable ically switched on or new electric consumers

in order to guarantee a stable and secure like electric vehicles start being charged.

energy supply. Smart Grids are defined as:

It further has to be acknowledged that the

Ean electricity network that can cost effi-

concept of Smart Grid does not refer to a

ciently integrate the behaviour and actions

of all users connected to it – generators, single technology, but is rather a set of differ-

consumers and those that do both – in or- ent technologies (cf. PEW 2009:1). Five key

der to ensure economically efficient, sus- technologies can be detected (cf. PEW

tainable power system with low losses and 2009:3f, cf. Levinson 2010:40f):

high levels of quality and security of supply

and safety. (M/490:2) (1) two-way communication that allows

real-time information flows and decision-

If the traditional electricity grid was cen- making among all grid components,

tralized in big generation utilities, today’s (2) sensing and measurement technolo-

picture has changed: Generation has be- gies that can monitor grid integrity and

come decentralized and is based on various congestion, equipment health and elec-

small units like photovoltaic (PV) cells of pri- tricity theft,

vate households or combined heat and pow- (3) transmission and storage components

er units (cf. Fuhr 2011:20). This creates the to make the infrastructure more efficient;

role of so-called prosumers: a term, which this includes high-temperature supercon-

recognizes the consumers’ emancipation ducting cables, distributed generation,

from traditional costumers to electricity pro- electricity storage, and transformers ca-

ducers and feeders (cf. DiStasio 2010:21). pable of remote monitoring,

(4) control devices and software to identi-

This implies that the grid’s flow direction fy and solve disruptions or outages, but

also changes. In a traditional electricity sys- also to process the gathered data and

tem, centrally generated electricity was fed provide it to human operators, and

into the transmission grid and passed on to (5) interfaces and decision support-tools

the distribution grid and reached the custom- to visualize networks and make them bet-

er through local networks. Future electricity ter manageable.

will be generated more decentralized and fed

in at the local level or at the distributional

8

According to a recent Greenpeace study for the Ger-

man energy sector nuclear energy could be phased-out

by 2015, and coal power stations by 2040 if new gas

power plants are installed as of 2011. The ambitious

goal is to rely on 100% RES by 2050 (cf. Greenpeace

2011a, cf. Umweltbundesamt 2010).

5MES-Perspektiven 01/2012

Figure 2 Electricity Flows in a Traditional and Future Electricity Network (own graph, based on

EnBW 2011).

Figure 3 Vision of a European Super Smart Grid (Energynautics 2011:9).

6MES-Perspektiven 01/2012

These technologies can enable a Smart assessment of its economic effects would

Grid whose characteristics then are (cf. exceed the scope of this study. A junior solu-

PEW 2009:4f): tion would be isolated national Smart Grids.

However, this cannot present more than a

(1) automated (and smart) meter reading, bridging solution, because the question of

(2) time variable tariffs such as real-time- international capacity markets and also the

pricing that reflects the dynamic market lifting of the immense potential of Scandina-

and could lead to price-elastic demand, vian wind energy or solar energy of Southern

(3) demand response which aims at re- countries are very viable.

ducing demand in peak times to avoid the

dispatching of expensive and often car-

bon-intensive peak capacities, 3. Research Question and Hypothesis

(4) vehicle to grid which includes smart

charging so that the electric vehicles can The research interest of this study is to quan-

either function as a feeder or a consumer tify the costs and benefits of a European

within the system – depending on the Smart Grid, because so far no specific re-

current load situation, and search on this very question exists. Figure 4

(5) distribution automation which would aims to visualize the specific approach of this

allow distribution systems “to reconfigure study: While the existing literature discusses

themselves when a fault occurs, restrict- numerous aspects of Smart Grids (bubbles of

ing the problem to a smaller area” (PEW the mind map), the research interest of this

2009:5) study can be understood as a complete se-

cond layer (blue cloud) that covers all these

aspects and adds a further dimension, with-

The question whether Smart Meters are an

out extensively discussing each smaller bub-

indispensable tool and whether they are con-

ble (for a detailed literature review see Chap-

stitutive for the establishment of a Smart Grid

ter 4.1). Therewith the inherent approach of

is contested. However, following the above-

this study is of a macro-analytic nature. Ac-

noted definition a Smart Grid needs to in-

cordingly, the specific research questions

clude all market participants. Consequently,

are:

the consumers have to be integrated into the

system9 In a larger perspective, a so-called

Super Grid is a macro grid, which focuses on RQ 1: Will the establishment of a Euro-

the power transmission across long distances pean Smart Grid be cost-effective?

(500km) and where innovative technologies

such as HVDC transmission become more RQ 2: How are the costs and benefits

important (cf. trend research 2009:67). Con- distributed among market actors?

sequently, a fully integrated European Smart

Grid would fulfil the definition of a Super RQ 3: What are the opportunity benefits

Smart Grid. of a Smart Grid compared to a Dumb

Grid adapted to integrate a high share of

RES?

The title of this study refers to a European

Smart Grid. As mentioned previously, a sin-

Concerning RQ2, distributional impacts are

gle European Smart Grid would entail im- generally not part of cost-benefit-analyses

mense and fundamental changes. Amongst (see also Chapter 5.1. However, it is as-

others a key issues is that the energy mix sumed that the costs of establishing a Smart

and the “general structure” of the member Grid are distributed very unevenly among

states energy system have not been commu- market actors. To be able to give clear and

nitarised yet (cf. TFEU Art. 194). Thus, as meaningful policy recommendations, it is

already discussed in Chapter 2.1, the objec- important to know which market actors profit

tive would be the deployment of a European most from the establishment of a Smart Grid

Smart Grid that consists of 27+2 intercon- and which market actors shoulder the highest

nected national Smart Grids including Nor- burden. Assumed that a high obstacle for

way and Switzerland (see Figure 3). Based realizing a Smart Grid is the reluctance of a

on the current EU legislation, the realization group of market actors to cover the neces-

of a single European Smart Grid and the sary investment costs, appropriate policy

recommendations must find ways of burden

9

The question remaining for further research is whether

a complete roll-out is efficient or whether smart substa-

tions would suffice.

7MES-Perspektiven 01/2012

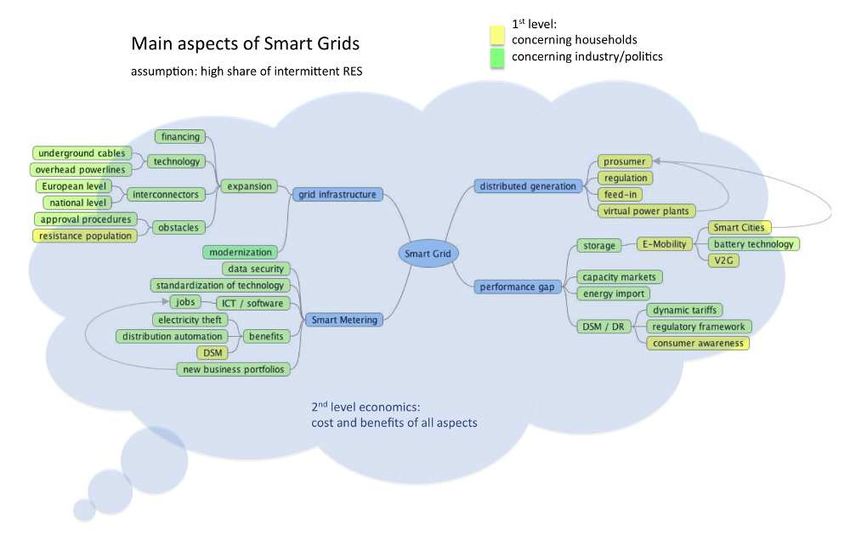

Figure 4 Main Aspects of Smart Grids and Added Value of This Paper (own graph)

sharing and incentive regulation for easing physical infrastructure, practically meaning

the establishment of a European Smart Grid. more cables need to be laid, because it will

not be able to rely on smart distribution of

In regard to RQ3, it is assumed that each intermittent energy through ICT and therewith

grid – be it smart or dumb – must be able to compensate peaks in supply or demand (see

integrate a high share of RES in the near Figure 5).

future. From that follows that also a Dumb

Grid has to be adapted to the integration of This leads to the formulation of the hypoth-

renewable energies. Consequently, Dumb esis guiding this study:

Grids also require major investments for ex-

panding and modernizing their infrastructure. The establishment of a European Smart

It is further hypothesized that these costs Grid will be worthwhile as the opportunity

exceed the costs of a Smart Grid, because a costs for adapting a Dumb Grid to the in-

Dumb Grid demands a larger amount of tegration of a high share of RES would

be even higher.

The EU Commission has already recognized

tremendous investments coming up. The

Commission estimates that EUR 1trn are

needed for modernizing the energy system

within the coming decade (cf.

COM(2010)677/4:9). An 80% roll-out of

Smart Meters by 2020 is further envisaged –

presuming the roll-out is assessed positively

(cf. 2009/72/EC, Annex 1). The Commission

acknowledges that the transition towards a

Smart Grid is a “complex issue and a single

Figure 5 Opportunity Benefits for Smart Grids leap from existing network to smart grids is

(own graph) not realistic”.

8MES-Perspektiven 01/2012

Hence, at this point the present study sary “symbiosis” (Edelmann 2010, see also

steps in, as “the benefits and costs of smart Hermsmeier 2010). For an overview of the

grids implementation will have to be objec- key features and technologies of Smart Grids

tively discussed and carefully explained, Hledik (2009) and Levinson (2010) offer a

through active participation of consumers, good synopsis. In the following the four main

small and medium enterprises and public debates will be outlined.

authorities” (COM(2010)677/4:40).

When integrating a significant amount of

4. State of Research RES into the grid, the existing infrastructure

has to be modernized. One discussion fo-

4.1. Literature Review cuses on the new energy flow introduced

through the increased integration of RES,

This section gives a review of the existing because energy from distributed generation

literature and research about Smart Grids. will be fed-in at the local grid, whereas tradi-

The state of research is twofold. On the one tionally centralized utilities fed-in at the distri-

hand, academia addresses the issue on an bution grid level. Second, the distribution

increasing basis , on the other hand concrete grids may become overloaded, because wind

economic analyses on the costs and benefits power will be generated mainly in the North-

of a Europe-wide Smart Grid are lacking. ern regions, whereas the consumption cen-

Until March 2011, there was no CBA that tres are located in the South (cf. Fuhr 2011).

analysed the cost and benefits of Smart The grid’s expansion as well as its regulation

Grids for a European perspective. There are is discussed by Jarass, Agricola, Kurth,

only 24 national CBAs, conducted by national Hirsbrunner, and Bauknecht. Kurth focuses

business consultancies, that either research on the problem of grid expansion – be it re-

the roll-out of Smart Metering or a Smart sistance in the population (also referring to

Grids deployment in a specific country. How- the BANANA-principle: “Build Absolutely

ever, the outcomes of the business cases Nothing Anywhere Near Anyone”) or lengthy

vary significantly and it is very hard to draw approval procedures (Kurth 2010). A “confus-

any conclusions about the relation between ing legal basis” of EU regulation on funding

assumptions and outcome of these studies for grid investments is another barrier

(see Chapter 5.3). (Hirsbrunner 2010). Consequently, different

regulatory instruments for a cost efficient grid

The topic of Smart Grids has gained operation and incentives for enhancing in-

enormous attraction only in the last few vestments in grid innovations are also dis-

years. In general, the research done so far is cussed (Bauknecht 2010). Wissner and Ha-

still elementary. In the German academic, the ber deal with appropriate system usage

journal “Energiewirtschaftliche Tagesfragen” charges for the modernized grid that has to

leads the debate. For an international per- be opened for the integration of distributed

spective, it is the journal “Energy Policy” that generated energy. Wissner argues that re-

gathers most of the publications. This litera- gional equalization payments have to be

ture review - as the whole study - concen- considered when designing the new system

trates on research concerning Smart Grids usage charges, since the electricity price

within a European perspective, while U.S. depends on the local energy source. From

and other case studies are excluded. this follows, that the higher the amount of

RES is, the more the prices will increase (cf.

The literature review follows the four main Wissner 2010). The technical details of the

components of Smart Grids developed in the infrastructure such as the pros and cons of

mind map: grid infrastructure, Smart Meter- overhead lines versus underground cables

ing, distributed generation, and performance are considered, too (cf. Merker 2010).

gap (see Figure 4). Further, this section is

organized by main ideas and not chronologi- The second main debate focusses on the

cally. There are also general contributions concept of Smart Metering. Förster (2010)

about Smart Grids focusing on the paradigm offers an overview of pros and cons of Smart

shift of the “new energy world” (Lamprecht Metering. Luckhardt present the hypothesis

2010), which will enhance a “new architec- that Smart Metering can become almost au-

ture” of electricity supply (Lambertz 2010). A tomatically cost-efficient through improved

broader perspective suggests that the in- process efficiency (Luckhardt 2010). This

crease of renewable energy sources and the assumption is backed up by Shekaras’s re-

establishment of Smart Grids are a neces- port about the reduction of electricity theft

9MES-Perspektiven 01/2012

through Smart Metering (cf. Shekara 2011). creates the profile of the so-called prosumer:

Gillich (2010) argues that the isolated roll-out it theorizes the costumers’ emancipation from

of Smart Meters will not bring benefits as traditional costumers to electricity producers

long as they are not integrated in the core and feeders (cf. DiStasio 2010). Cossent

processes of energy suppliers and develops underlines that various regulatory issues

the concept of Smart Billing. Feuchtmeier such as charges, services and incentives

(2010) elaborates that a European wide need to be revised and clarified (cf. Cossent

standardization of the Smart Meter software 2009). Distributed generation enhances the

is out of question. According to that Hand- establishment of so-called virtual power

schuh (2010) sees the main restraints of plants. There within, the virtual pooling of

Smart Meters in missing standards and a distributed generating resources could help

lack of costumer awareness and willingness to outbalance the intermittency of RES (cf.

to cooperate. Another discussion focuses on Niehörster 2010). Lueddeckens (2011) fo-

the new business portfolios and services that cuses on the cost-efficiency of virtual power

can be introduced with Smart Metering plants.

(Bechmann 2010, DiStasio 2010, Levinson

2010, Oesterwind 2010). The fourth debate about how to cope with

the intermittency of renewables entails the

Smart Metering is very closely connected question of how to bypass the performance

to the topic of Information and Communica- gap – an incident that appears in a combina-

tion Technology (ICT) (cf. Drossel 2011, tion of peak times and calm weather condi-

Koenig 2010). Wissner develops the hypoth- tions (cf. Edenhofer 2008). There are four

esis that investment in ICT is necessary to ways to overcome this problem: by providing

exploit potentials in all stages of the energy peak load capacity, by importing energy, by

value chain. He further argues that all parts establishing storage systems and/or Demand

of smart life – be it grids or appliances or Side Management (cf. Rehtanz 2011). An-

meters – only smart through ICT (Wissner other thread within this debate is the so-

2011a and 2011b). This entails the discus- called transnational capacity markets that

sion about data security and data protection. would add a market for capacities to the con-

In Cavoukian’s opinion Smart Metering will ventional formation of prices via the merit-

entail a “data explosion”, which has to be order-curve (cf. Nailis 2011). Another solution

based on strict data protection measures, to avoid performance gaps are storage sys-

because if the consumers fear about their tems that aim at storing electricity in times

personal data the whole Smart Grid devel- where supply surpasses demand. Speaking

opment will fail as consumers are a crucial of pump storage, water is pumped in an

component of its success (Cavoukian 2009). above-situated lake in times of over genera-

Cavoukian also develops the Privacy by De- tion and rushed down propelling a turbine in

sign model, whereby the design of data ap- times of a supply gap. In this regard, the hy-

plications already decides about fundamental pothesis circulates that politics overestimate

aspects of data protection. In contrast, Beyea the role of storage as “ultimate response”. In

acknowledges the huge potential of this im- contrast Gatzen (2011) holds the opinion that

mense new database for epidemiologic re- storage would only be meaningful with a sim-

search: “The simultaneous response of mil- ultaneous grid expansion. Wade (2010) con-

lions of customers to episodic weather centrates on the benefits of energy storage

changes, national tragedies [E] could be such as voltage control and power flow man-

studied by social scientists. Comparisons agement. Also new technologies like com-

across countries could be fascinating” (Beyea pressed air reservoirs are discussed in litera-

2010). Knyrim (2011) comments on this topic ture (cf. Fuhr 2011). Electric vehicles are

from a legal perspective for the EU and the considered to be another possibility of stor-

U.S. age. Galus develops three steps of integrat-

ing E-Mobility as a storage capacity: uncon-

Third, the question of distributed genera- trolled charging without communication with

tion is tackled by many publications. The the system, controlled charging (vehicle gets

traditional electricity generation happened in power from the grid when supply is suffi-

centralized utilities, today’s picture is very cient), and the smartest solution the often-

different: generation has become decentral- cited vehicle to grid (V2G) where the vehicle

ized and is based on various small units like not only is charged but can also feed power

PV cells of private households or combined back into the system (cf. Galus 2010, Twick-

heat and power units (cf. Fuhr 2011). This

10MES-Perspektiven 01/2012

ler 2010). This further entails the vision of building capacities for an integration of a high

whole Smart Cities (cf. Lindauer 2011). RES-share into the European electricity grid.

Further targets of the action plan are: the

As a further means to control demand, strengthening of an internal energy market,

Demand Side Management focuses on bal- the adoption of a strategic energy technology

ancing peaks by incentivizing the costumers plan, as well as the objective of a low carbon

to reduce their demand in peak times or shift future including CCS and the improvement of

the demand to off-peak times through flexible the Emission Trading Scheme (ETS) (cf.

tariffs (cf. Gillich 2010, Hermsmeier 2010, COM(2007)1). These objectives – to increase

Haber 2010). Faruqui argues that dynamic the share of RES and reduce energy con-

tariffs could “make or break” the pay-off from sumption through efficiency measures – aim

Smart Meters in the EU (Faruqui 2010a). to strengthen climate protection, but also to

This is very closely interlinked with another ensure the EU’s energy supply (cf. TFEU Art.

discussion that acknowledges the customers’ 194 lit.b).

willingness and awareness as necessary

condition for the success of Smart Grids. The Energy and Climate Package fol-

Faruqui underlines that the costumer en- lowed in 2008; it is made up of four directives

gagement is the “sina qua non of success” and one regulation. Its legal basis is the pro-

for Demand Side Management (Faruqui motion of energy efficiency and energy sav-

2010b). ing as well as the development of RES (cf.

TFEU Art.194 lit.c). The directives aim at the

The literature review shows that the ques- allowance trading system, ETS (cf. COM

tion of the economic effects of a European (2008)16), the effort of the member states to

Smart Grid is not extensively researched and meet the GHG emission reduction commit-

that it is worth examining the research ques- ments, effort sharing (cf. COM(2008)17), the

tions developed in Chapter 3. geological storage of carbon dioxide, CCS

(cf. COM(2008)18), as well as the promotion

4.2 State of Politics of the use of energy from RES (cf.

COM(2008(19). Additionally, the regulation

sets emission standards for new passenger

This section gives an overview of the legal cars (cf. EC/443/2009). In this way the Ener-

basis for the establishment of a European gy and Climate Package implements the

Smart Grid, starting with the current state of

objectives of the action plan. However, this

policies in the EU and closing with an over-

legislative package supports the EU’s strate-

view of those six countries chosen as case

gy, but does not further bring substantial

studies in the analysis.

changes for a Smart Grid policy. The follow-

ing policies can be classified into three differ-

European Level ent groups: liberalization, technology, and

infrastructure.

Basic Decisions: the 20-20-20 targets and

the Energy and Climate Package Liberalization Policies

In 2007, the European Council confirmed its

First, concerning the creation of an internal

intention to limit the global average tempera-

energy market for electricity and gas. The

ture increase to 2°C above pre-industrial

first and second energy package aimed to

levels and announced an integrated ap-

render the energy markets in the EU com-

proach for a common climate and energy

petitive10, based on Art. 194 TFEU. This has

policy (cf. 7224/1/07, no.27f).

led to the establishment of independent na-

tional regulatory authorities in order to moni-

This entailed the Communication An En- tor network companies and suppliers 11. In this

ergy Policy for Europe that provides the basis context, the EU also aims at improving the

for all policies to follow. It comprises – inter infrastructure to guarantee an efficient

alia – the 20-20-20 targets: 20% reduction of transport of energy.12 The Third Energy Mar-

GHG emissions, 20% share of RES, and

20% more energy efficiency by 2020 (cf. 10

COM(2007)1). In the context of this study Cf. URL DG Energy: Internal Market. What do we want

to achieve?

especially the intention to increase the share

11

of renewables in the European energy mix to Cf. ibid.

20% until 2020 is a major driving force for 12

Cf. ibid.

11MES-Perspektiven 01/2012

ket Liberalization Package introduced, steps easily. The EU aims at covering 20% of its

to further liberalize the European energy electricity consumption through wind energy

market. It focuses on unbundling the electrici- by 2020 and 15% by solar energy (cf. ibid).

ty networks from the vertically integrated The electricity grid initiative names three

power companies13 The third energy package objectives: first, creating a real internal ener-

also creates ACER, the Agency for the Co- gy market, second integrating “a massive

operation of Energy Regulators, in order to increase of intermittent energy sources” and

strengthen the power and independence of third managing “complex interactions be-

national regulators (cf. DG Energy 2011:2f). tween suppliers and costumers” (COM(2009)

Together with ENTSO, the European Net- 519:5). The goal is that 50% of the European

work of Transmission System Operators, networks would enable the “seamless inte-

they shall have a key role in developing tech- gration of renewables and operate along

nical rules at EU level (cf. DG Energy ‘smart’ principles, effectively matching supply

2011:9). Annex I of the third energy package and demand” (ibid). CCS technology shall be

states that the member states shall ensure widely commercialized, so that the target of

that customers are actively engaged in the having an “almost zero carbon power genera-

electricity supply market through “intelligent tion” is met by 2050 (COM(2009)519:6).

metering systems” (2009/72/EC, Annex 1).

As of 2020, 80% of consumers shall be Infrastructure Policies

equipped with smart meters in case the roll-

out “is assessed positively” (ibid.). The

Commission does not further define what a Third, the legislation concerning the grid in-

positive assessment means – a term that is frastructure is based on the treaty provision

even broader than ‘cost-effective’. A study for that the EU policy shall aim at promoting the

the German sector concludes that a roll-out interconnection of energy networks (cf. TFEU

of Smart Meter is only worthwhile for 43% of Art. 194 lit.d). The EU shall further contribute

the households at maximum (cf. Frontier to the “establishment and development of

2011:20). trans-European networks in the areas of

transport, telecommunications and energy

infrastructures” (TFEU Art. 170,1). The TEN-

Technology Policies E legislation on trans-European energy net-

works aims at the interconnection and in-

Second, concerning the technologies, the teroperability of the European energy net-

SET-Plan (Strategic Energy Technology works: the internal energy market shall be

Plan) wants to enhance the development of operated effectively, the isolation of island

low carbon technologies in the EU (cf. regions reduced, the security of energy sup-

COM(2007)723). Its legal basis is also the plies reinforced and environmental protection

functioning of the energy market (cf. TFEU promoted (cf. 1364/2006/EC Art.3). The deci-

Art. 194 lit. a). The according 2009 technolo- sion foresees that the European electricity

gy roadmap – which puts the SET-Plan in networks shall be adapted and developed in

concrete terms – sets out industrial initiatives order to “facilitate the integration and connec-

to promote investments. The interesting ones tion of renewable energy production” (cf.

for the research interest of this study are the 1364/2006/EC, Art.4,22). This decision also

European wind initiative, the solar Europe initiates the so-called projects of common

initiative, the European electricity grid initia- interest, which create a priority financing

tive, and the European CCS initiative (cf. mechanism for cross-border projects “without

COM(2009)519 and SEC(2009)1295). Wind local benefits” (cf. 1364/2006/EC, Art.6,1.

and solar energy shall become more cost- COM(2010)677/4:11).

effective, and shall be fed into the grid more

The Second Strategic Energy Review

contains six priority infrastructure actions for

13

Member states can choose between three different modernizing the European grid and envisions

unbundling models: ownership unbundling (TSO owns a smart interconnected electricity network

and manages the network, the supplier has no control,

no voting rights, and only minority shareholding), ITO until 2050 (cf. COM(2008)781). The Com-

(TSO owns and operates the network, but the vertically mission acknowledges that “huge changes”

integrated utility has a supervisory body, independent have to be made to adapt the European elec-

management and a compliance officer), ISO (ISO oper- tricity grid to decentralized generation, and is

ates the network, but the vertically integrated utility owns

the network and leased it to ISO) (cf. URL DG Energy: supportive of the roll-out of Smart Meters (cf,

The 3rd Energy Package and its main measures). COM(2008)781:16). It even envisions an

12MES-Perspektiven 01/2012

“offshore supergrid ring around Europe to dures for infrastructure projects (ibid.). Ac-

connect southern solar, western wave and cording to the Commission, more than ten

northern wind” (cf. COM(2008:781):16). It years lay between the planning and final

further claims the will of a “zero-carbon elec- commissioning of a power line in Europe (cf.

tricity supply for the EU by 2050” (cf. ibid, COM(2011):8). For the electricity sector the

p.17). The strategic energy review can be resulting delays would prevent “50% of com-

seen as basis for all related communications mercially viable projects from being realized

following after 2008. by 2020” (COM(2010)677/4:8). The Commis-

sion also names priority corridors for infra-

The Communication “Energy 2020 – A structure projects. They are (1) an offshore

strategy for competitive, sustainable and grid in the Northern Seas and connection to

secure energy” states a pan-European inte- Northern as well as Central Europe, (2) inter-

grated energy market as a priority and connections in South Western Europe, (3)

acknowledges that between 2010 and 2020 connections in Central Eastern and South

about EUR 1trn will be needed to make “Eu- Eastern Europe, and (4) completion of the

rope’s installations and infrastructures fit for Baltic Energy Market Interconnection Plan

the future” (Oettinger 2011b:1). The commu- (cf. COM(2011)677/4:10f, see Figure 6).

nication wants to foster the implementation of

the internal market legislation, the establish- Task Force Smart Grids

ment of a blueprint for the European infra-

structure 2020-2030 (see COM(2010)677/4), Finally, in 2009 the Commission launched –

the streamlining of permit procedures and under the provisions of the third energy

market rules for infrastructure developments, package – the Task Force for Smart Grids,

and the provision of a financing framework which sees the evolution of the electricity grid

(cf. COM(2010/639:11f). as a “key challenge” for Europe’s electricity

This led to the Communication “Energy in- networks.14 In its mission, the Task Force

frastructure priorities for 2020 and beyond – underlines two priorities: the roll-out of Smart

A Blueprint for an integrated European ener- Meters in the EU since a “main feature” of

gy network”. According to Commissioner establishing a Smart Grid would be to turn

Oettinger, Europe is going through a para- customers to active market participants.15 In

digm shift in the way the EU produces, comparison to the third energy package the

transmits, distributes, and trades energy:

“Our existing grid is simply not up to the chal-

lenge. It has to be updated; it is too old, too

fragmented, and already overloaded at sev-

eral critical points” (Oettinger 2011a:3). The

investment needs of EUR 1trn also includes

EUR 500bn investments in transmission net-

works “including electricity and gas distribu-

tion and transmission, storage, and smart

grids” (cf. COM(2010)677/4:9). The Commis-

sion further estimates that only half of these

investments will “be taken up by the market”

– creating an investment gap of about EUR

100bn (ibid.). But the Commission also re-

marks that the opportunity costs would be

even higher (cf. ibid). This communication

also calls attention that electricity grids not

only have to be updated to be able to inte-

grate a high share of RES, but that – despite

all efforts to increase energy efficiency –

electricity demand is increasing because of

“the multiplication of applications and tech-

nologies relying on electricity as an energy Figure 6 Priority Corridors for Electricity, Gas

and Oil (COM(2010)677/4:20)

source (heat pumps, electric vehicles, hydro-

gen and fuel cells, information and communi- 14

URL DG Energy, Task Force Smart Grids: Vision and

cation devices etc.)” (COM(2010)677/4:6). Work Programme, p.1

The communication also refers to the obsta- 15

cle of “long and uncertain” permitting proce- URL DG Energy, Task Force Smart Grids: Mission,

p.1.

13Sie können auch lesen