Sachstand Steuerliche Förderung von Forschung und Entwicklung in den OECD-Staaten - Wissenschaftliche Dienste

←

→

Transkription von Seiteninhalten

Wenn Ihr Browser die Seite nicht korrekt rendert, bitte, lesen Sie den Inhalt der Seite unten

Wissenschaftliche Dienste Sachstand Steuerliche Förderung von Forschung und Entwicklung in den OECD-Staaten © 2016 Deutscher Bundestag WD 4 - 3000 - 102/16

Wissenschaftliche Dienste Sachstand Seite 2

WD 4 - 3000 - 102/16

Steuerliche Förderung von Forschung und Entwicklung in den

OECD-Staaten

Aktenzeichen: WD 4 - 3000 - 102/16

Abschluss der Arbeit: 07. September 2016

Fachbereich: WD 4: Haushalt und Finanzen

Die Wissenschaftlichen Dienste des Deutschen Bundestages unterstützen die Mitglieder des Deutschen Bundestages

bei ihrer mandatsbezogenen Tätigkeit. Ihre Arbeiten geben nicht die Auffassung des Deutschen Bundestages, eines sei-

ner Organe oder der Bundestagsverwaltung wieder. Vielmehr liegen sie in der fachlichen Verantwortung der Verfasse-

rinnen und Verfasser sowie der Fachbereichsleitung. Arbeiten der Wissenschaftlichen Dienste geben nur den zum Zeit-

punkt der Erstellung des Textes aktuellen Stand wieder und stellen eine individuelle Auftragsarbeit für einen Abge-

ordneten des Bundestages dar. Die Arbeiten können der Geheimschutzordnung des Bundestages unterliegende, ge-

schützte oder andere nicht zur Veröffentlichung geeignete Informationen enthalten. Eine beabsichtigte Weitergabe oder

Veröffentlichung ist vorab dem jeweiligen Fachbereich anzuzeigen und nur mit Angabe der Quelle zulässig. Der Fach-

bereich berät über die dabei zu berücksichtigenden Fragen.

Wissenschaftliche Dienste Sachstand Seite 3

WD 4 - 3000 - 102/16

Inhaltsverzeichnis

1. Fragestellung 4

2. Vorgehen 4

3. Übersicht über die Steueranreize zur Förderung von

Forschung und Entwicklung in den OECD-Staaten 4

4. Details der Steuerfreibeträge und Steuergutschriften in

den OECD-Staaten 6

5. Lizenzboxen 29

6. Wirkung der Förderung von Forschung und Entwicklung 32

Wissenschaftliche Dienste Sachstand Seite 4

WD 4 - 3000 - 102/16

1. Fragestellung

Steuerliche Förderung von Forschung und Entwicklung in den OECD Ländern mit folgenden As-

pekten: Wo gibt es diese Förderung, wie sehen die Möglichkeiten dort aus und gibt es Erkennt-

nisse über die Wirkung?

2. Vorgehen

Der nachfolgende Sachstand beginnt mit einer tabellarischen Übersicht über die steuerlichen An-

reize zur Förderung für Forschung und Entwicklung in den Mitgliedstaaten der Organisation für

wirtschaftliche Zusammenarbeit und Entwicklung (OECD). Als steuerliche Anreize gewähren die

Mitgliedstaaten Steuerfreibeträge und Steuergutschriften1, einen erhöhten Ausgabenabzug (Super

Deduction) und Lizenzboxen.2 Ausnahmen bilden Mexiko, das Zuschüsse zu Forschungs- und

Entwicklungsausgaben aus einem Fonds gewährt, und Schweden, wo die Vergünstigung über ei-

nen Abzug bei den Sozialversicherungsbeiträgen erfolgt, sowie Deutschland und Estland.

Im weiteren Verlauf des Sachstands werden zunächst die Steuerabzüge und dann die Lizenzbo-

xen detaillierter vorgestellt. Der Sachstand schließt mit einer Studie über die Wirkung der Förde-

rung von Forschung und Entwicklung.

3. Übersicht über die Steueranreize zur Förderung von Forschung und Entwicklung in den

OECD-Staaten

Der nachfolgenden Tabelle liegt die Darstellung in PwC Global R&D Incentives Group vom Feb-

ruar 2016 zugrunde.3 In Europa gewähren nur Deutschland und Estland keinerlei steuerliche För-

derung.4

Steuerabzüge und Erhöhter Ausgabenabzug Lizenzbox

–gutschriften („Super Deduction“)

Australia X

Austria X

Belgium X X X

1 Steuerfreibeträge verringern die steuerliche Bemessungsgrundlage, Steuergutschriften („tax credits“) werden

direkt von der Steuerschuld abgezogen.

2 Auch Patent- bzw. Innovationsboxen oder IP Boxes (intellectual property boxes), im Folgenden immer Lizenz-

box.

3 PricewaterhouseCoopers: Global Research & Development Incentives Group, Februar 2016, Seite 6, unter:

https://www.pwc.com/gx/en/tax/pdf/pwc-global-r-and-d-brochure-feb-2016.pdf, abgerufen am 01. Septem-

ber 2016.

4 European Commission, Taxation Papers: A Study on R&D Tax Incentives, Final Report, 28. November 2014,

Working Papers No. 52 – 2014, Seite 5, unter: https://ec.europa.eu/futurium/en/system/files/ged/28-taxud-

study_on_rnd_tax_incentives_-_2014.pdf, abgerufen am 07. September 2016.

Wissenschaftliche Dienste Sachstand Seite 5

WD 4 - 3000 - 102/16

Steuerabzüge und Erhöhter Ausgabenabzug Lizenzbox

–gutschriften („Super Deduction“)

Canada X X5

Chile X

Czech Republic X

Denmark X

Finland X

France X X

Greece X

Hungary X X X

Iceland X

Ireland X X

Israel X X

Italy X X

Japan X

Korea X X

Latvia X

Luxembourg X

Mexico (grants)

Netherland X X

New Zealand X

Norway X

Poland X

Portugal X X

Slovak Republic X

Slovenia X

Spain X X

Sweden (exemption of social

security contributions)

Switzerland X (Canton Nidwalden)

Turkey X X X

United Kingdom X X X

United States X

5 Deloitte: R&D tax update: Canada’s first patent box regime – an incentive for domestic R&D commercialization,

28. April 2016, unter: https://www2.deloitte.com/content/dam/Deloitte/ca/Documents/tax/ca-en-RD-16-1-pa-

tent-box-AODA.PDF, abgerufen am 05. September 2016.Wissenschaftliche Dienste Sachstand Seite 6

WD 4 - 3000 - 102/16

4. Details der Steuerfreibeträge und Steuergutschriften in den OECD-Staaten

Das Directorate for Science, Technology and Innovation der OECD erstellt umfangreiche Doku-

mentationen und Übersichten mit verschiedenen Schwerpunkten zur steuerlichen Förderung von

Forschung und Entwicklung in ihren Mitgliedstaaten. Das sehr umfassende und sehr detaillierte

„Compendium of R&D Tax Incentive Schemes“ wurde zuletzt am 17. Dezember 2015 aktuali-

siert.6

Um jedoch einen Überblick zu vermitteln, der auch Vergleiche zulässt, basiert der nachfolgende

Sachstand auf der Zusammenstellung der PwC Global R&D Incentives Group vom Februar 2016.7

Diese Zusammenstellung wurde nochmals modifiziert, um bessere Lesbarkeit herzustellen. Die in

der Zusammenstellung von PwC nicht vorhandenen Daten für Chile, Finnland, Griechenland,

Neuseeland, Norwegen, Slowenien und Schweden sind dem oben genannten OECD-Kompen-

dium entnommen. Beide Publikationen liegen ausschließlich auf Englisch vor.

6 OECD: Compendium of R&D Tax Incentive Schemes: OECD Countries and selected economies, 17. Dezem-

ber 2015, unter: https://www.oecd.org/sti/rd-tax-incentives-compendium.pdf, abgerufen am 01. Septem-

ber 2016.

7 PricewaterhouseCoopers: Global Research & Development Incentives Group, Februar 2016, unter:

https://www.pwc.com/gx/en/tax/pdf/pwc-global-r-and-d-brochure-feb-2016.pdf, abgerufen am 01. Septem-

ber 2016.Wissenschaftliche Dienste Sachstand Seite 7

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

Australia 1. 45% refundable Based on volume Yes - if grouped turnover Non-refundable R&D tax Discreet grant funding

R&D tax offset for groupedWissenschaftliche Dienste Sachstand Seite 8

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

Austria. The premium is Promotion Agency (FFG),

not capped. An application Municipalcredit (KPC),

for approval has tobe filed Austrian Tourism Bank

electronically after the end (ÖHT), Austrian Control

of each fiscal year to obtain Bank (OeKB), EC – Incen-

confirmation from the Aus- tives (e.g. Horizon 2020)

trian Research Promotion and several federal state

Agency (FFG) that the R&D promotion companies

activities performed by a

company meet the neces-

sary criteria.

2. For subcontracted

R&D that is placed by an

Austrian entity or perma-

nent establishment with a

subcontractor located in

the EU or EEA, a 10% vol-

ume-based tax credit may

also be claimed on all qual-

ified R&D related expendi-

ture. The subcontracted

R&D premium is capped

with a maximum base

amount of EUR 1,000,000

p.a., hence a total R&D pre-

mium of EUR 100,000. Fur-

ther the subcontractor

must not be under the con-

trolling influence of the

hiring company and there

should not be a tax group

in place between the hiringWissenschaftliche Dienste Sachstand Seite 9

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

company and the subcon-

tractor.

According to the Tax Re-

form 2015/16, which is to

become effective as of 1

January 2016, the research

premium is to be increased

from 10% to 12%.

Belgium • One-time R&D in- Based on volume of invest- Yes, if the incentive is Unused R&D investment • 13.5% (*) investment de-

vestment deduction of ment in qualifying R&D as- claimed in the form of an deduction/R&D tax credit duction on acquisition

13.5% (*) of the acquisi- sets (including capitalised R&D tax credit, the remain- is carried forward for an value of qualifying patents

tion value of qualifying R&D expenses) ing balance of unused R&D unlimited period. • Special expat tax status

R&D investments tax credits after five tax for foreign researchers tem-

• Spread R&D invest- years is paid to the com- porarily assigned to Bel-

ment deduction of 20.5% pany. gium

(*) of the depreciation on • 80% payroll withholding

qualifying R&D Invest- tax exemption. The exemp-

ments tion is assigned to qualify-

• The above incen- ing research programs.

tives can be claimed in the • Specific advantageous re-

form of an R&D tax credit gime for qualifying SMEs

which corresponds to the that qualify as young inno-

R&D investment deduc- vative companies

tion, multiplied by the

• Regional R&D grants

standard corporate tax rate

available,which are exempt

of 33.99%

from corporate income tax

(*)Rate for financial years

• Notional interest deduc-

ending between 31 Decem-

tion for equity funded R&D

ber 2014 and 30 December

activities

2015 (included)Wissenschaftliche Dienste Sachstand Seite 10

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

(*)Rate for financial years

ending between 31

December 2014 and 30 De-

cember 2015

(included)

Canada 1. 20% non-refundable fed- Credit on volume • Federal credits are re- Unused non-refundable • 65% uplift on eligible

eral tax credit on qualified fundable for certain Cana- federal and provincial tax salary based expenditures.

expenditures. Reduced to dian controlled private cor- credits may be carried for- Uplift reduced to 60% for

15% after 2013. Certain Ca- porations. ward 20 years or carried 2013, and to 55% after

nadian controlled private • Certain of the provincial back 3 years 2013

corporations are eligible credits are refundable. • Certain federal and pro-

for the 35% refundable vincial direct funding pro-

credit on the first $3 mil- grams may be available for

lion of qualified expendi- R&D activities

tures; and

• R&D capital expenditures

2. Provincial tax credits, attract 100% tax deprecia-

ranging from 4.5% to tion in the year available

37.5%, certain of which for use. Repealed for years

are refundable after 2013

Chile 35% tax credit and 65% al- Volume based Where an exess tax credit Accelerated depreciation

lowance arises, it can be carried for R&D machinery and

Ceiling: Yearly cap of over to the future tax years buildings.

15,000 UTM (Monthly tax (not exist a limit of years).

unit; approximately

CLP$570 million)

Czech Re- 200/210% super deduction 200% super deduction on No. Non-utilised allowance Investment incentives

public volume, may be carried forward 3 available for setting up/ex-

210% super deduction on years pansion of: (i) production

increment facilities, (ii) technological

centres (the R&D allowance

cannot be used for projectsWissenschaftliche Dienste Sachstand Seite 11

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

that are supporter by an-

other form of public sup-

port). There are also vari-

ous grants for R&D or inno-

vation.

Denmark 1. Danish tax law allows Volume based. Yes, see “tax incentive/re- Tax losses may be carried • Foreign researchers hired

for an immediate write-off lief“ item 2 concerning tax forward indefinitely. by a Danish company may

of capital expenditures for credits. Denmark applies a mini- benefit from a significantly

R&D. Alternatively, the mum taxation rule such reduced income tax rate for

taxpayer may choose to that tax losses carried for-5 years.

take tax depreciation in the ward can reduce taxable • Grant funding available

same year and the follow- income exceeding DKK

ing four years on a straight- 7.7475 million with 60%

line basis. only. Taxable income up to

2. Companies have been a threshold of DKK 7.7475

granted the opportunity to million can be off set in

apply to the Danish tax au- full by tax losses carried

thorities for a payment forward. Unused tax losses

equal to the tax value of may be utilized in later in-

negative taxable income re- come years.

lating to R&D costs up to

DKK 25 million.

Tax payments according to

this rule cannot exceed an

amount of DKK 5.875 mil-

lion (the tax value of DKK

25 million at tax rate of

23.5 %) in 2015.

In 2016 the tax rate is low-

ered to 22 % implying thatWissenschaftliche Dienste Sachstand Seite 12

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

the tax payment cannot ex-

ceed an amount of DKK 5.5

million.

For companies subject to

tax consolidation, the limit

of DKK 25 million applies

for the tax consolidation

group in total.

3. Costs related to purchase

of patents and know-how

(including rights/licenses

to utilize patents or know-

how) may either be fully

expensed in the year of ac-

quisition or amortized over

a seven-year period.

Finland 100% tax deduction: Volume based. 10 years

Minimum threshold of

EUR 15.000 in terms of eli-

gible amount of R&D

Ceiling of EUR 400.000 in

terms of eligible amount of

R&D. The maximum an-

nual net benefit gained by

a company is EUR 80,000

in 2014.

100% tax relief on any sal-

ary expenses for R&D activ-

ity related to their own

business operationsWissenschaftliche Dienste Sachstand Seite 13

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

France • 30% rate up to €100m el- Credit on volume. Yes. Excess credits may be car- The R&D tax credit tax rul-

igible expenses ried forward 3 years. Any ing process has been ad-

• 50% rate up to €100m el- unused tax credit is re- justed as from 1st January

igible expenses for over- fundable at the end of this 2013: a tax ruling could be

seas territory. three year period. As an requested from the French

exception, excess credits tax authorities to confirm

• 5% credit in excess of

are immediately refunda- the eligibility of the R&D

€100m eligible expenses

ble to certain qualifying projects launched during a

• Scope of the R&D tax companies. given year. The tax ruling

credit has been extended to request in this respect shall

some innovation expendi- be filed no later than six

tures such as prototypes, months before the R&D tax

design and pilot plants for credit filing deadline (i.e.

new products incurred by by mid- November 2015 for

small and medium-size en- R&D expenses incurred in

terprises. For said ex- 2015).

penses, the credit rate is

20%, and applies to a max-

imum of €400,000 of inno-

vation expenses (i.e. as-

sessment basis)

• French Tax Authorities

(FTA) have published new

guidelines on subcontract-

ing expenses t and public

subsidies and staff ex-

penses that have tough-

ened the regime

Germany No. No. No. No. R&D projects can count on

numerous forms of finan-

cial support. There are

many programs allocatingWissenschaftliche Dienste Sachstand Seite 14

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

R&D grants, interest-re-

duced loans, and special

partnership programs. Fi-

nancing is provided by the

European Union (EU), the

German government, and

the individual German

states.

Funding ranges from 25%

to 50% of eligible costs for

industrial research pro-

jects. Specific limitations

are defined in the relevant

call for projects.

Greece 30% tax deduction 5 years

Hungary • 200% “super deduction” Deduction on volume. No. Yes. If R&D costs are capi- State and EU sponsored

• 10-year tax allowance for talized as intangible assets, grants for R&D purposes

certain investments made the amortization on these are also available.

for research projects with assets is deductible during Direct own R&D costs can

present value of at least the amortization period. also be deducted from the

HUF 100 million (approx. from the base of the Hun-

EUR 350,000) available up garian local business tax

to 80% of the calculated (tax rate is maximum2%of

corporate income tax lia- the net sales revenue, de-

bility creased by the material

costs, direct costs of R&D,

costs of subcontractors'

work, and certain part of

costs of goods sold and

costs of mediated services)

and innovation contribu-

tion (tax rate is 0.3% of theWissenschaftliche Dienste Sachstand Seite 15

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

base of the local business

tax).

The Hungarian government

established the Hungarian

Intellectual Property Office

("HIPO"). This organization

is authorized to issue bind-

ing rulings in order to

identify whether future

R&D project of Hungarian

companies qualifies as

R&D projects. The HIPO

acts as an advisor in assis-

tance with the Tax Author-

ity regarding retrospective

R&D project as well.

Iceland Large firm and SME 20% Volume based. N/A

of personnel costs, cost of

tools and equipment,

buildings and land, costs

associated with contractual

research, technical

knowledge and patents

Minimum: ISK 1 million

per project

Ceiling: ISK 100 million

per project and firm (150

million in the case of pur-

chased R&D or collabora-

tion agreement)Wissenschaftliche Dienste Sachstand Seite 16

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

Ireland 25% tax credit plus a trad- Volume based. Yes. Excess credits may be re- Various government grant

ing reduction of 12.5% to funded or carried forward incentives for establishing

give an effective overall re- indefinitely or expanding R&D activi-

duction of 37.5% ties in Ireland, e.g., capital,

employment, training, fea-

sibility, pilot

projects, etc.

For accounting periods

commencing from 1 Janu-

ary 2012, companies who

are in receipt of an R&D tax

credit will now in certain

instances have the option

to reward key employees.

Israel R&D expenses shall be de- Based on volume of invest- No. Tax loss generated from 1. When R&D costs are

ducted in the tax year in- ment in qualifying R&D as- R&D deductions can be borne by a taxpayer that is

curred when such expense sets. carried forward indefi- not the owner of an enter-

has been approved as an nitely. prise performing the R&D,

R&D expense by the rele- or, the taxpayer partici-

vant government depart- pates in R&D costs of an-

ment . The approval in re- other developer in consid-

gard to industrial related eration for a reasonable re-

projects is generally turn, and when such R&D

granted by the Office of the projects also enjoy govern-

Chief Scientist mental grants, the R&D ex-

("OCS").When such OCS penses incurred shall gen-

approval is not obtained, erally be deducted over

the expense shall be de- two tax years. The deducti-

ducted over three tax ble expenses allowed to a

years. participant in R&D costs of

another developer gener-

ally may not exceed 40%Wissenschaftliche Dienste Sachstand Seite 17

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

of the taxable income of

the taxpayer in the year in

which the expenses were

incurred.

2. R&D Grants - Companies

can be provided with cer-

tain grants for R&D activi-

ties according to the R&D

Law, subject to a prior ap-

proval of the OCS.

3. “The Angels Law” - A

single taxpayer which his

investment in an R&D com-

pany complies with differ-

ent criteria, can deduct his

investment as an expense

over maximumof 3 years.

The total tax benefit shall

not exceed approximately

USD 1.25M.

Italy Tax credit equal to: Based on incremental R&D The credit is non-refunda- Not specifically stated, Accounting documentation

• 25% of the incremental investments respect to the ble, it can be used to offset therefore is reasonable that must be certified by an au-

expenses related to ma- average of the R&D ex- tax debts without any limi- the credit may be carried ditor.

chinery and laboratory penses sustained in FYs tation. forward indefinitely. R&D tax credit incentives

equipment used for the 2012, 2013, 2014. Newco can be added to Patent Box

R&D; credit is computed on the Regime.

base of the total amount of

• 50% of the incremental

the R&D expenses.

expenses related to R&D

qualified employees and The incentive is in force

external qualified R&D up to FY 2019.

contracts.Wissenschaftliche Dienste Sachstand Seite 18

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

The credit cannot exceed €

5.000.000 per year.

MinimumR&D expense

amount must be equal to €

30.000.

Japan 1. Maximumcredit of 25% 1. Credit on volume No. Certain excess credits may Government bodies pro-

of total tax liability (plus 2. Temporal credit on in- be carried forward 1 year. vide various grants for R&D

5% of special R&D cost cremental spending until (Note) Due to the 2015 Tax activities.

based credit, i.e., joint R&D the fiscal year beginning Reform, carry-forward is SpecialMeasures for the

with or contracted R&D by before 1 April 2017 no longer applicable. Promotion of R&D by Certi-

university or public re- fied Multinational Enter-

search institution, etc.) for prises.

a fiscal year beginning

from April 1, 2015.

2. Additional and temporal

10% credit.

Korea 1. Tax credit to the extent Credit on either incremen- No. Excess credits can be car- 1. Investment tax credit on

of either (i) 2% to 3% tal or volume. ried forward 5 years. facilities for the purpose of

(25% for Small & Medium However, the incremental R&D and job training up to

Enterprises; SMEs, 8% for method cannot be used in 3% to 10% such invest-

Medium-scale Companies ; case of either (i) no R&D ment. These rates are dif-

MSCs, 15% or 10% for the expense has been incurred ferentiated by the company

intermediate stage from during the previous four size. In other words, a 3%

SMEs to MSCs) of the cur- years or (ii) the R&D ex- tax credit would apply to

rent R&D expenses or (ii) penses of last year are less large companies while 5%

40% (50% for SMEs) of the than the average of the pre- and 10% would apply to

incremental portion of the vious four years MSCs and SMEs respec-

current R&D expenses over tively.

the amount of

last year.Wissenschaftliche Dienste Sachstand Seite 19

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

2. R&D tax credit for core

technologies as authorised

by government ministries

as well as pre designated

strategic growth industries:

20% (30% for SMEs) of the

current expenditures.

Latvia 300% super -deduction is Volume based. No. R&D costs are deductible 1. Prior to starting a new

applied for qualifying R&D in the tax period they are R&D project taxpayer

costs (with the exception incurred regardless of should perform certain ac-

of depreciation and amorti- whether a taxable profit or tivities - e.g. define the ob-

sation charges) - e.g., tax- loss is reported for the pe-jectives of the project.

payers can claim a corpo- riod. describe the scientific or

rate income tax (CIT) de- Any tax loss arising after technological uncertainty,

duction for their R&D ex- the deduction of R&D costs which is expected to be re-

penses multiplied by a co- can be carried forward in- solved as well as the ex-

efficient of 3. definitely. pected innovation etc.

Further description of

If the R&D costs are capi-

these activities must be ad-

talised they are deductible

ded to project documenta-

according the period used

tion , which will be revie-

for depreciation for finan-

wed by State commission

cial purposes

to apply the tax incentive.

2. If R&D projects were

subsidized by the State or

EU grants , tax incentive

may not be applied.

Mexico No. No. No. No. The Mexican Government

provides complementary

financial support for the

R&D projects developed

inMexico on annual basisWissenschaftliche Dienste Sachstand Seite 20

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

to promote competitive-

ness and innovation. The

funds usually grant a per-

centage of the investment

spent mainly in the follow-

ing concepts: training, ac-

quisition of specialized

equipment, human re-

sources, specialized con-

sulting fees (foreign and lo-

cal), IP protection strategy,

trials, pilot and prototype

expenses.

The National Council of

Science and Technology

(CONACyT) is the Mexican

authority in charge of

granting funds with refer-

ence to R&D activities,

however, there are other

funding options according

to State or Sector.

One important aspect to

consider, is that once a

project is favoured by one

Fund, it cannot receive any

further support from the

Mexican Government, for

the same phase/stage/activ-

ities.

Netherland • R&D credit (above the Volume based. No. No. Several grants are available

line) for qualifying R&D for R&D, mostly through aWissenschaftliche Dienste Sachstand Seite 21

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

wages, investments and ex- sectoral approach (e.g.,

penses: 32% for the first ICT, Life Science, Chemis-

Euro 300k and 16% on the try) and provide up to 50%

excess amount (known as cash grants for eligible

WBSO) cost.

• Corporate tax deduction

for IP development costs at

once.

New Zea- 28% tax credit

land It is the smallest of: - NZD

500,000 multiplied by the

corporate tax rate; - the

company’s net loss for the

year multiplied by the cor-

porate tax rate; - the com-

pany’s research and devel-

opment expenditure for the

tax year multiplied by the

corporate tax rate; or - the

company’s total research

and development labour

expenditure for the year,

multiplied by 1.5 and also

multiplied by the corporate

tax rate. The first cap of

NZD500,000 increases by

300,000 for the next five

years after 2015. In tax year

2020-2021, the cap will be

maintained at 2M.IWissenschaftliche Dienste Sachstand Seite 22

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

Norway 18% tax credit for large Volume based

firms

20% tax credit for SME

The credit is subject to an

annual limitation per pro-

ject per company

Poland Additional tax deduction Volume No. Yes. Possibility to carry • grants for R&D projects

of R&D costs incurred: forward the tax credit for 8 aimed at developing new

• 30% - R&D personnel years if you are in a tax- products and

salaries, loss position in current technologies

year

• 20% for SME’s for other • cash grants for R&D

R&D costs (e.g. deprecia- works and commercializa-

tion, R&D services, raw tion of innovative

materials) environmentally-friendly

• 10% for large entities for technologies, allowing also

other R&D costs (e.g. de- for financing

preciation, R&D services, the investment stage of a

raw materials) project

Since 2017 the above lim- • opportunity to benefit

its are expected to grow – from cash grants dedicated

amended bill under negoti- to industrial

ations - (up to 50% of sala-

research and development

ries and 30%for other R&D

works conducted within

costs)

the particular

sectors (separate schemes

available for aviation sec-

tor, medicines,

gaming industry, drones,

chemistry, textile, steel –

other underWissenschaftliche Dienste Sachstand Seite 23

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

negotiations)

• co-financing of costs in-

curred by filing a patent

application

• possibility to obtain gov-

ernmental cash grants for

creation of R&D

centers (under construc-

tion)

• cash grants for the sci-

ence and industry sector

within the scope of

applied research in various

scientific fields

Portugal SIFIDE Combination of volume No. Possibility to carry forward There’s a financial grant

Tax Credit = 0,325Dn + and incremental based the tax credit for 8 years (6 program available (cumula-

0,5[Dn - (Dn-1 + Dn-2)/2)] years until 2013). tive with R&D tax credits)

Where D stands for the

amount of R&D expenses

incurred each year, net of

non-reimbursable financial

Government contributions.

Slovak Re- 1. Cash subsidies for R&D Incremental. No. No. Other grants for R&D are

public projects from the state accessible via EU funds.

budget

2. Income tax relief – at the

amount incurred on R&D

within the project for

which incentives were ap-

provedWissenschaftliche Dienste Sachstand Seite 24

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

Slovenia 100% Volume based 5 years

Ceiling: Amount of the tax

base

Spain 1. 25% credit plus 1. credit on volume plus Yes. It is possible under Excess credits may be car- Autonomous regions pro-

2. 42% credit plus 2. credit on incremental in- certain circumstances, to ried forward 18 years vide additional business

ask for a cash-refund for incentives; tangible and in-

3. 8% credit on certain as- crease plus

the amount of unused R&D tangible fixed assets, ex-

set acquisitions 3. credit on volume for

tax credits up to €3 mil- cluding buildings, used for

4. 17% certain staff salaries technological innovations lion. R&D activities may be

(industrial design and pro-

5. 12% credit on techno- freely depreciated

duction process engineer-

logical innovation.

ing)

4. credit on volume for

technological Innovations

Sweden Partial exemption of social

security contributions:

Social security charges are

currently rated at 31.42%.

The reduction of the con-

tribution amounts to 10%

of the net salary of the R&D

employee.

Work at least 75% of its

working hours on R&D and

at least 15 hours per

month. Be aged between 25

and 64 (at the beginning of

the year when the reduc-

tion is claimed; prior to

May 2015, the applicableWissenschaftliche Dienste Sachstand Seite 25

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

age bracket ranged from 26

to 65 years).

SSC deductions capped at

SEK 230000 per month and

company/group (or SEK

2.76 mn. per year).

Switzerland Future R&D expenses are N/A N/A N/A N/A

to a certain extent tax de-

ductible (by booking a re-

spective provision).

Tax deductibility for future

R&D expenses is limited to

10% of the annual taxable

profit and capped at CHF

1Mio. This is incentive is

only available for future

R&D expenses relating to

3rd parties.

Turkey R&D Law No.5746: Incremental No. Any unutilized R&D de- • Grants funding by sev-

• All eligible innovation duction can be carried for- eral governmental institu-

and R&D expenditures ward without any time tions for eligible R&D pro-

made in R&D centres, tech- limitation, indexed to the jects

nology centres, R&D and revaluation rate which is • Other grants for R&D are

innovation projects sup- an approximation of infla- accessible via EU funds

ported by governmental in- tion rate.

• Corporate income tax ex-

stitutions, foundations es- emption

tablished by law or inter-

• R&D deduction

national funds.

• Income tax exemption

• 100% R&D deduction

over the eligible innova- • Social security premi-

umsupportWissenschaftliche Dienste Sachstand Seite 26

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

tion and R&D expendi- • Stamp tax exemption

tures. The same expendi- • VAT exemption (only for

tures can also be capital- delivery of software and

ised and expensed through services)

amortisation over five

years.

• Companies with separate

R&D centres employing

more than 500 R&D per-

sonnel can – in addition to

the above deduction – de-

duct half of any increase in

R&D expenditures over

R&D expenditures in the

previous period.

• 80% (90% for personnel

with a PhD degree) of the

salary income of eligible

R&D and support person-

nel is exempt from income

tax.

• Half of the employer por-

tion of social security pre-

miums for R&D and sup-

port personnel are funded

by the Ministry of Finance.

• Documents prepared in

relation to R&D activities

are exempt from stamp

duty.Wissenschaftliche Dienste Sachstand Seite 27

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

Technology Development

Zones Law No.4691:

• Profit derived from the

software development ac-

tivities or research and de-

velopment activities in

techno parks is exempt

from corporate income tax

until 31 December 2023.

• The salaries of R&D and

support personnel working

in techno parks are exempt

from income tax.

• Half of the employer por-

tion of social security pre-

miums for R&D and sup-

port personnel are funded

by the Ministry of Finance.

• Deliveries of certain

types of software (system

management, data manage-

ment, business application,

sector-specific, internet,

mobile and military com-

mand control application

software) produced by the

companies operating in

techno parks are exempt

from 18% VAT.Wissenschaftliche Dienste Sachstand Seite 28

WD 4 - 3000 - 102/16

Steueranreize/ Förderung des Ausgaben- Auszahlbarkeit Vortragsmöglichkeit Zuschüsse/Sonstiges

Steuererleichterungen zuwachses (incremental)/

Förderung Summe Ausga-

ben (volume)

United “Super deduction”: Deduction on volume Large companies – A cash Extra deduction reduces Expenditure on assets used

Kingdom Large Companies credit is available from 1 taxable profits. If a loss re- for R&D attracts 100% tax

April 2013 under the new sults this can be carried depreciation in the year of

• from 1 April 2013 option

10% R&D expenditure forward indefinitely, offset acquisition. Regional

to claim the 10% Research

credit. There is no ability current profits (including grants are available.

& Development expendi-

to receive a cash credit un- other UK group compa-

ture credit (RDEC) instead

der the super-deduction re- nies) and offset prior year

of 130% super deduction.

gime which is still availa- profits.

• from April 2016 RDEC ble instead of the new Large company RDEC -

will be mandatory. credit until 2016. loss making companies - it

• the RDEC is payable to SMEs – ability to surrender is possible to carry forward

lossmaking companies. losses for cash back – as- any withheld tax and ex-

Small and medium Enter- suming sufficient losses, cess credit due to re-

prises(SMEs): effective cashback is strictions

• 175% pre 1 April 2011 24.75% (cashback rate of

11% on a super deduction

• 200% from 1 April 2011

of 225%). For expenditure

to 31 March 2012

incurred from 1 April

• 225% from 1 April 2012 2014, the effective cash-

back has increased to

32.625% (cashback rate of

14.5% on a super deduc-

tion of 225%).

United 20% Credit (regular Credit on incremental No. Excess credits may be car- States provide R&D credit

States method) spending, with limitations ried back 1 year and for- in addition to various busi-

14% Credit (Alt. Simpli- Credit on incremental ward 20 ness incentives. In addi-

fied Credit) spending, without Limita- tion to the credit, R&D ex-

tions penditures are deductible

in determining taxable in-

come.Wissenschaftliche Dienste Sachstand Seite 29

WD 4 - 3000 - 102/16

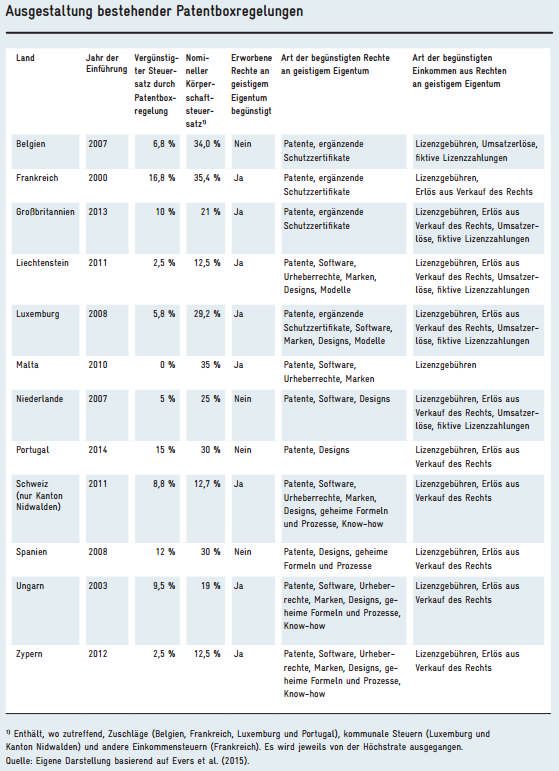

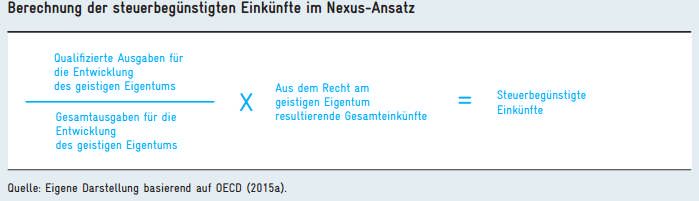

5. Lizenzboxen

Lizenzboxen stellen einen Steueranreiz dar, weil sie bestimmte Einkünfte aus der Verwertung

immaterieller Wirtschaftsgüter wie Patente, Marken oder Urheberrechte weitgehend von der Be-

steuerung freistellen. Einerseits versprechen sich Staaten davon mehr Investitionen in Forschung

und Entwicklung. Andererseits besteht die Gefahr, dass multinationale Unternehmen Lizenzbo-

xen im Rahmen von Steuerplanungsmodellen nutzen.8 Die OECD hat sich deshalb im Rahmen

des BEPS-Projekts9 beim Umgang mit Lizenzboxen auf den „Nexus-Ansatz“ verständigt. Die Ex-

pertenkommission Forschung und Innovation führt aus, dass beim Nexus-Ansatz die wesentliche

Geschäftstätigkeit an den Ausgaben festgemacht wird. Es ist jedoch nicht der Absolutbetrag der

Ausgaben entscheidend, sondern der Anteil der qualifizierten Ausgaben an den Gesamtausgaben

für die Entwicklung des geistigen Eigentums. Dieser Anteil bestimmt, in welcher Höhe die Ge-

samteinkünfte, die aus dem Recht am geistigen Eigentum resultieren, dem vergünstigten Steuer-

satz unterliegen. Die qualifizierten Ausgaben für die Entwicklung des geistigen Eigentums müs-

sen direkt beim Steuerpflichtigen angefallen sein. Sie umfassen nur Ausgaben, die für die tat-

sächlich durchgeführten Forschungs- und Entwicklungs-Tätigkeiten notwendig sind. Ausgaben,

bei denen kein direkter Zusammenhang zu spezifischen Rechten an geistigem Eigentum besteht,

können nicht angerechnet werden (zum Beispiel Zinszahlungen, Baukosten, Anschaffungskos-

ten). Die genaue Definition dieser Ausgaben obliegt den einzelnen Staaten. Als Formel stellt sich

der Nexus-Ansatz wie folgt dar:10

8 Evers, Lisa: Unternehmensbesteuerung: Europäische IP Box Regime in der Kritik, Zentrum für Europäische

Wirtschaftsforschung (ZEW), ZEW News Januar/Februar 2015, Seite 6, unter: http://ftp.zew.de/pub/zew-

docs/zn/zn0215.pdf, abgerufen am 05. September 2016. Der Begriff „Box“ kann zum einen daher kommen, dass

bestimmte Einkünfte in einer Gruppe (Box) zusammengefasst und separat besteuert werden. Es kann sich aber

auch vom Kästchen (Box) im Steuerformular ableiten, das anzukreuzen ist, wenn solche Einkünfte bestehen,

vgl. Belitz, Heike: Steuerliche Förderung von Forschung und Entwicklung – Erfahrungen aus dem Ausland,

Deutsches Institut für Wirtschaftsforschung DIW Roundup 85 vom 23. November 2015,

http://www.diw.de/sixcms/detail.php?id=diw_01.c.520333.de, abgerufen am 07. September 2016.

9 BEPS steht für Base Erosion and Profit Shifting, auf deutsch etwa Gewinnkürzung und Gewinnverlagerung. Das

BEPS-Projekt wurde mit dem Ziel initiiert, gegen den schädlichen Steuerwettbewerb der Staaten und aggressive

Steuerplanungen international tätiger Konzerne vorzugehen, vgl. Bundesministerium der Finanzen: Fragen und

Antworten zum Abschluss des BEPS-Projekts, unter: http://www.bundesfinanzministerium.de/Con-

tent/DE/FAQ/2014-06-05-faq-beps.html, abgerufen am 06. September 2016.

10 Expertenkommission Forschung und Innovation: Gutachten zu Forschung, Innovation und technologischer

Leistungsfähigkeit Deutschlands 2016, Seite 25, unter: https://www.bmbf.de/files/EFI_Gutachten_2016.pdf, ab-

gerufen am 06. September 2016.Wissenschaftliche Dienste Sachstand Seite 30

WD 4 - 3000 - 102/16

Lizenzboxen nach altem System müssen bis zum 30. Juni 2021 geändert worden sein.11

Die nachfolgende Tabelle gibt einen Überblick, in welchen europäischen Staaten Lizenzboxen zu

welchen Bedingungen existieren.12 Die Tabelle ist ergänzt um weitere OECD-Staaten, die mit

Stand Februar 2016 über Lizenzboxen verfügen.13

11 OECD/G20 Base Erosion and Profit Shifting Project, Action 5: Agreement on Modified Nexus Approach for IP

Regimes, unter: https://www.oecd.org/ctp/beps-action-5-agreement-on-modified-nexus-approach-for-ip-re-

gimes.pdf, abgerufen am 06. September 2016.

12 Expertenkommission Forschung und Innovation: Gutachten zu Forschung, Innovation und technologischer

Leistungsfähigkeit Deutschlands 2016, Seite 23, unter: https://www.bmbf.de/files/EFI_Gutachten_2016.pdf, ab-

gerufen am 06. September 2016.

13 Basierend auf: PricewaterhouseCoopers: Global Research & Development Incentives Group, Februar 2016, Seite

6, unter: https://www.pwc.com/gx/en/tax/pdf/pwc-global-r-and-d-brochure-feb-2016.pdf, abgerufen am 01. Sep-

tember 2016.Wissenschaftliche Dienste Sachstand Seite 31

WD 4 - 3000 - 102/16Wissenschaftliche Dienste Sachstand Seite 32

WD 4 - 3000 - 102/16

Weitere Staaten mit Lizenzboxen

Vergünstigter Steuersatz

Staat Jahr der Einführung durch Patentboxregelung

Irland Dezember 2015 6,25% qualifying profits

2004 9%/16% according to the

Israel geographic location

2014 5~11% (Sale of IP)

Korea 7,5~16,5% (Royalty)

2015 (2001 in Technology 10%

Türkei Development Zones)

6. Wirkung der Förderung von Forschung und Entwicklung

Eine umfangreiche Studie zur Wirkung von steuerlichen Anreizen bei Forschung und Entwick-

lung in verschiedenen Staaten hat die Europäische Kommission bei mehreren Forschungsinstitu-

ten unter Federführung des CPB Netherlands Bureau for Economic Policy Analysis in Auftrag ge-

geben.14 Ausgewertet wurden Studien in den einzelnen Staaten, sofern dort eine Erhebung auf

wissenschaftlicher Basis überhaupt stattgefunden hat. Eine Zusammenfassung der Ergebnisse

dieser Studie findet sich im DIW Roundup 85 vom 23. November 2015: 15

– Ökonometrisch anspruchsvollere Studien kommen zu dem Ergebnis, dass für einen Euro

steuerlicher Anreiz ein Zuwachs der Ausgaben von Forschung und Entwicklung von weni-

ger als einem Euro erreicht wird.

– Die steuerliche Förderung führt zwar zu mehr inkrementellen Innovationen, ist aber keine

Voraussetzung für radikale Innovationen.

– Die steuerliche Förderung sollte an Forschungsausgaben anknüpfen, die am ehesten Über-

tragungseffekte („spill over-Effekte“) hervorbringen. Dazu gehören insbesondere Personal-

kosten, weil Forscher zwischen Unternehmen wechseln und ihr Wissen mitnehmen.

– Junge Unternehmen bringen eher radikale Innovationen hervor und fordern damit etablierte

Unternehmen heraus. Auch die OECD empfiehlt die steuerliche Förderung junger Unter-

nehmen, die nicht die Möglichkeit grenzüberschreitender Steueroptimierung haben.

14 European Commission, Taxation Papers: A Study on R&D Tax Incentives, Final Report, 28. November 2014,

Working Papers No. 52 – 2014, unter: https://ec.europa.eu/futurium/en/system/files/ged/28-taxud-

study_on_rnd_tax_incentives_-_2014.pdf, abgerufen am 07. September 2016.

15 Belitz, Heike: Steuerliche Förderung von Forschung und Entwicklung – Erfahrungen aus dem Ausland, Deut-

sches Institut für Wirtschaftsforschung DIW Roundup 85 vom 23. November 2015,

http://www.diw.de/sixcms/detail.php?id=diw_01.c.520333.de, abgerufen am 07. September 2016. In diesem

Beitrag finden sich auch Hinweise auf andere Studien und Publikationen, auch auf die OECD Science, Techno-

logy and Industry Outlooks („STI Outlooks“).Wissenschaftliche Dienste Sachstand Seite 33

WD 4 - 3000 - 102/16

– Steuerliche Verlustvorträge und unmittelbare Rückerstattungen kommen insbesondere klei-

nen Unternehmen zugute, die noch nicht oder zeitweise nicht profitabel sind.

– Die Bewerbung um steuerliche Förderung sollte für Unternehmen einfach und die Bedin-

gungen transparent sein (Online-Anträge, zentrale nationale Anlaufstellen – one stop).

Das DIW Roundup fasst zudem die Vor- und Nachteile der steuerlichen Forschungs- und Ent-

wicklungsförderung vor dem Hintergrund der Diskussion in Deutschland zusammen und weist

auf die EU-Beihilferechts-Vorschriften bei Einführung steuerlicher Fördermaßnahmen hin.

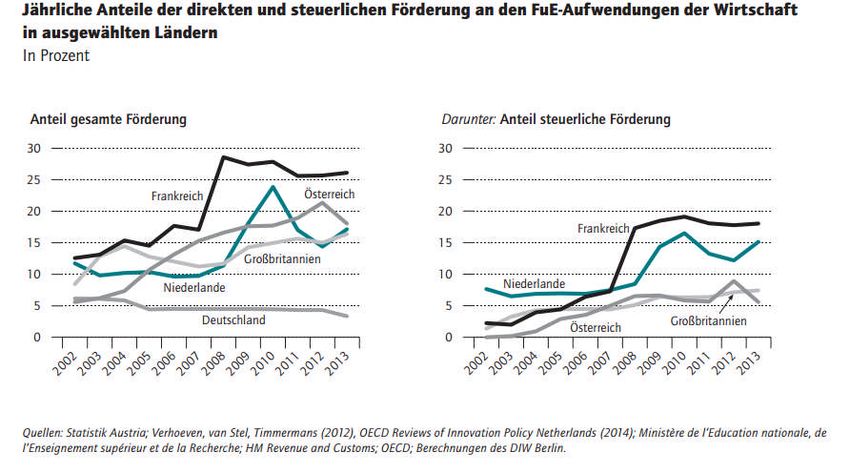

Dieselbe Autorin vom DIW hat sich 2016 noch einmal mit der Effizienz der Förderung von For-

schung und Entwicklung in den OECD-Länder befasst.16 Dabei misst sie die Fördereffizienz auf

gesamtwirtschaftlicher Ebene, indem der jährliche Zuwachs beziehungsweise die Abnahme der

selbst finanzierten FuE-Aufwendungen der Unternehmen eines Landes (ohne die Fördermittel) in

Relation zu den gesamten Fördermitteln in einem Jahr gesetzt werden.

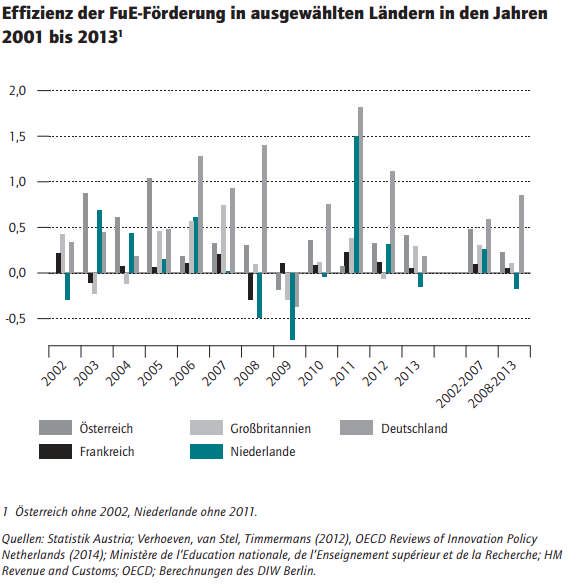

Ein Effizienzwert von 1 oder darüber bedeutet, dass Fördermittel in Höhe von einem Euro mit

zusätzlichen selbst finanzierten FuE-Aufwendungen der Unternehmen von einem oder mehr als

einem Euro im selben Jahr einhergehen. Ein Wirkungsgrad über Null und unter 1 zeigt an, dass

jedem Euro an Fördermitteln weniger als ein Euro zusätzlicher privater FuE-Aufwendungen ge-

genüberstehen. Bei einer Fördereffizienz von Null oder weniger sind die selbst finanzierten FuE-

Aufwendungen trotz Förderung nicht gestiegen oder sogar gesunken („crowding out“).

Die Ergebnisse für Deutschland, die Niederlande, Großbritannien, Österreich und Frankreich

sind in den folgenden Grafiken zusammengestellt:

16 Belitz, Heike: Förderung privater Forschung und Entwicklung in OECD-Ländern: immer mehr, aber auch immer

ineffizienter, in: DIW Wochenbericht 8/2016, unter: https://www.diw.de/sixcms/de-

tail.php?id=diw_01.c.527689.de, abgerufen am 07. September 2016.Wissenschaftliche Dienste Sachstand Seite 34

WD 4 - 3000 - 102/16Wissenschaftliche Dienste Sachstand Seite 35

WD 4 - 3000 - 102/16

Die letzte Grafik zeigt, dass gut Dreiviertel der jährlichen Fördereffizienzwerte zwar größer als

Null sind, davon aber gut die Hälfte kleiner als 0,5. Ein Euro Förderung bedeutet somit einen An-

stieg der von den Unternehmen selbst finanzierten Forschungs- und Entwicklungsaufwendungen

um weniger als 0,5 Euro. Nur 22 Prozent der Effizienzwerte sind kleiner als Null, sie treten ge-

häuft in der Zeit der weltweiten Finanzkrise auf. Die Mittelwerte der Fördereffizienz sind im

Zeitraum vor dieser Krise (2002 bis 2007) meistens höher als danach (2008 bis 2013). Dies deutet

auf eine sinkende Fördereffizienz bei gestiegenen Förderquoten in den europäischen Vergleichs-

ländern hin. Ausnahme ist Deutschland, wo nicht nur die höchste gesamtwirtschaftliche För-

dereffizienz erreicht wird, sondern auch kein Rückgang im Zeitraum nach der Krise zu beobach-

ten ist. Nach Ansicht der Autoren lassen die Ergebnisse daran zweifeln, dass hohe und in einigen

Ländern stark gestiegene Förderquoten, die oft mit einer Ausweitung der breiten steuerlichen

Förderung einhergingen, einen wirkungsvollen Beitrag zur Erhöhung der Forschung und Ent-

wicklung in den Unternehmen geleistet haben.17

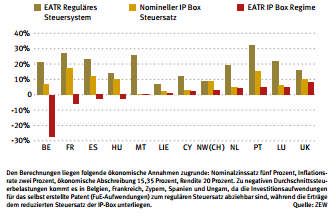

Zur Wirkung von Lizenzboxen hat das Zentrum für Europäische Wirtschaftsforschung (ZEW) in

2015, also vor der Einigung über ein einheitliches Lizenzbox-Regime auf OECD-Ebene, eine Stu-

die vorgelegt. Die nachfolgende Grafik zeigt die effektive Durchschnittssteuerbelastung (effective

average tax rates - EATR) einer Investition in ein selbsterstelltes Patent. In allen europäischen

Staaten mit Lizenzboxen sinkt die effektive Durchschnittssteuerbelastung deutlich, was inner-

halb der Studie zu dem Schluss führt, dass Lizenzboxen offensichtlich einen Anreiz für Investiti-

onen setzen.18

- Ende der Bearbeitung -

17 Belitz, Heike: Förderung privater Forschung und Entwicklung in OECD-Ländern: immer mehr, aber auch immer

ineffizienter, in: DIW Wochenbericht 8/2016, Seite 156f., unter: https://www.diw.de/sixcms/de-

tail.php?id=diw_01.c.527689.de, abgerufen am 07. September 2016.

18 Evers, Lisa: Unternehmensbesteuerung: Europäische IP Box Regime in der Kritik, Zentrum für Europäische

Wirtschaftsforschung (ZEW), ZEW News Januar/Februar 2015, Seite 6, unter: http://ftp.zew.de/pub/zew-

docs/zn/zn0215.pdf, abgerufen am 07. September 2016.Sie können auch lesen